|

| Chart I - Milk Production through August - 23 States |

Florida is a good indicator of fluid milk consumption changes, as almost all of Florida's milk is for fluid consumption. Because fluid milk cannot be held for a long time, it is impossible to build an inventory of fluid milk. What is produced is consumed quickly.

For years Florida's milk was the highest paid milk in the country because Class I milk for drinking is the highest paid milk and Florida's milk is almost all Class I milk. Now Florida has to contend with a rapidly shrinking market for their milk. The milk produced in Florida (Chart II) has been declining at an increasingly fast rate topped by August's decline of 7.8% vs. the prior year.

|

| Chart II - Florida Milk Production Decline January to August 2018 |

|

| Chart III - Florida Cow Decline January to August 2018 |

States other than Florida are less influenced by the declining consumption in beverage milk. Milk volumes going to growth products like cheese temper other states decline in beverage milk. As an example, the Upper Midwest milk goes mostly to cheese, so it is minimally impacted by the decline in fluid milk consumption. The milk supply in Wisconsin is up 1.4% in August over the prior year, which is slightly below the current growth rate for cheese consumption.

What states are growing in milk production? Texas, Kansas, and Colorado are growing in milk production. Texas is now the fifth largest dairy state. Its milk production has grown by 12% since the start of 2017. In August Texas produced 1.1 billion pounds of milk. If the growth rate continues, they could pass New York and Idaho to become the third largest milk producing state in the U.S. behind only California and Wisconsin.

States with shrinking milk production in August include Virginia at -4.3%, Vermont, at -3%California at -2.3%, Michigan at -1.3%, New Mexico at -0.8%, Pennsylvania at-0.7%, Illinois at -0.6%, Oregon at -0.5%, and Ohio at -.02%. Most all of these states have a significant amount of declining fluid milk in their portfolios.

The overall message on where the dairy industry is going is getting increasingly clear. Class I beverage milk is declining and the trend appears to be accelerating. Because Class I is the highest paid milk, the overall average price (the "uniform" price) will also decline. This, in-turn, will have implications on the producer price differentials, which will also decline and that may lead to further de-pooling.

There is still too much milk in the system and that is being channeled to cheese because it can be inventoried for a longer period of time. The high cheese inventories will keep the cheese price low and therefore the Class III milk price will remain low.

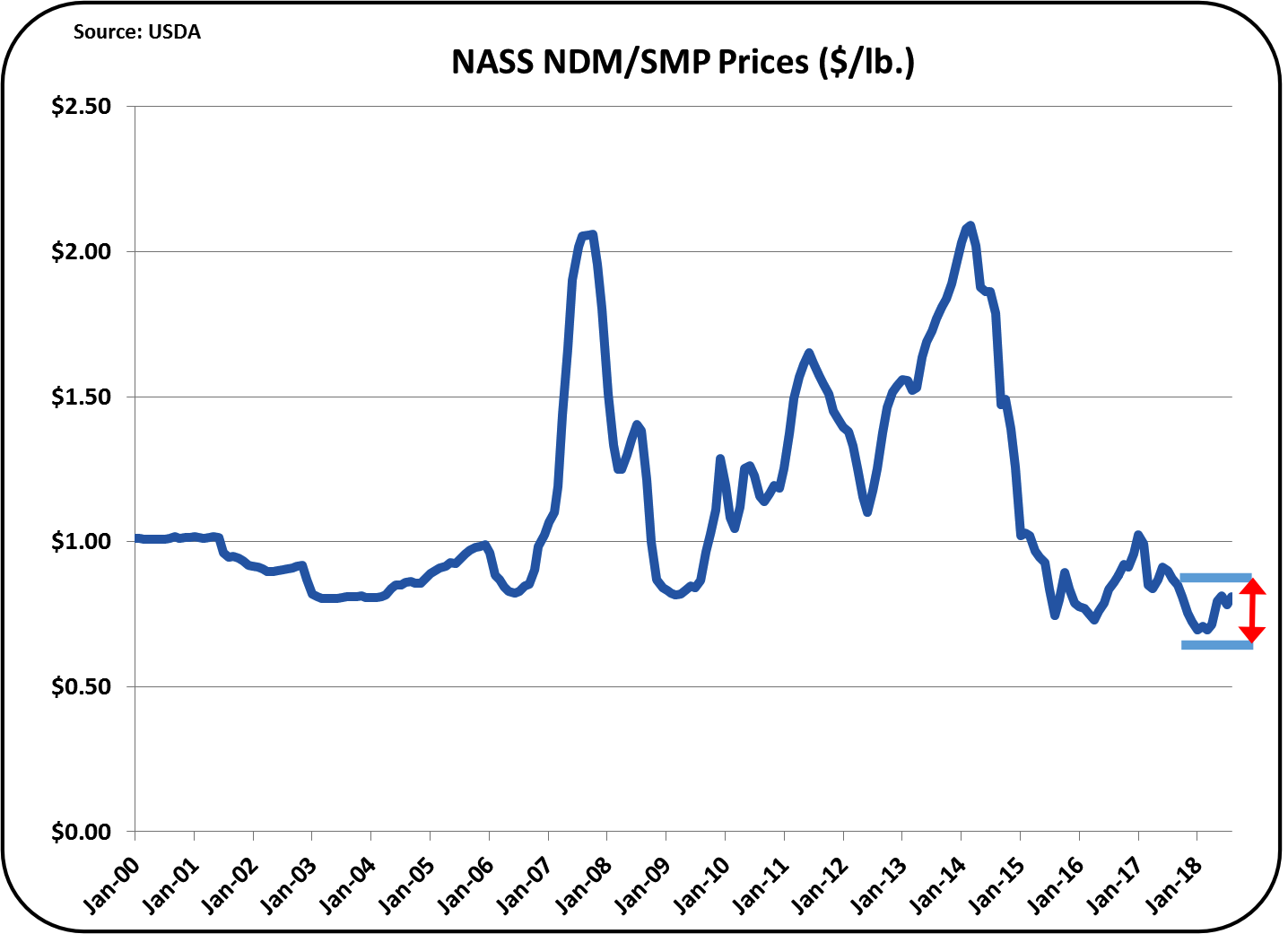

Although butter was not specifically covered in this post, the continued increase in the consumption of butter will also lead to excess nonfat dry milk/skimmed milk powder, keeping Class IV milk prices low. Overall, it appears that milk prices will remain "status quo."