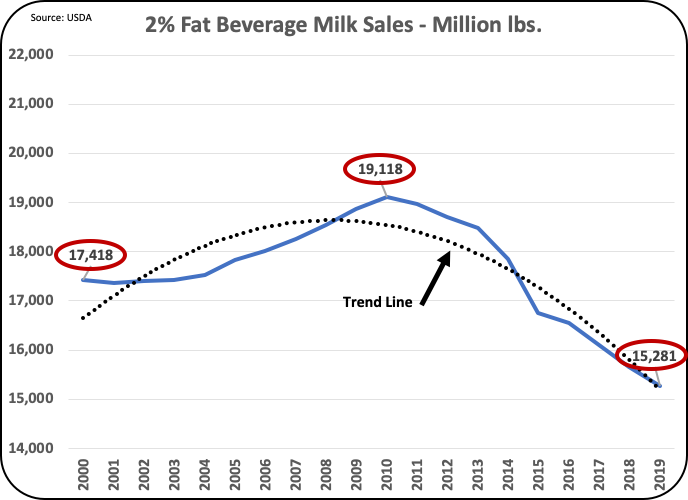

In the prior post, the latest statistics on domestic consumption of dairy products was reviewed. This post will analyze the supply side needed to match this demand.

The USDA summary of domestic consumption, which is based on percent butterfat in each of the dairy products, indicates an increased need for milk of roughly two percent annually based on the trends from the last five years. The consumption data for individual sectors showed cheese and butter demand growing while fluid milk and yogurt were falling.

Data for the year 2020 has been extremely volatile as the impact of COVID-19 and quarantining have skewed the numbers significantly. By 2021, a more normal pattern should evolve. Unlike the very quick changes brought on by COVID-19, the recovery will likely be a much slower and provide a more manageable transition. The production of milk has not been significantly influenced by COVID=19

Milk production over the last ten years in the U.S. is shown in Chart I. This chart is based on 12-month moving averages over the last 10 years. The 12-month averages are used to reduce seasonal and monthly variations.

As can be seen, the increase in milk volume produced has been long-term and steady. Over the 10-year span shown in Chart I, milk production has increased by 1.4 percent annually. With these long-term trends, a continuation of this increase is very likely.

|

| Chart I - Milk Production by Month |

The number of cows that were used for this level of production is shown in Chart II. The number of cows increased steadily until 2018. Between the start of 2018 and mid 2019 the number of cows decreased by 1.3 percent. Since then the number of cows has started to increase again.

|

| Chart II - Number of U.S. Dairy Cows in the U.S. |

Milk per cow is shown in Chart III. There has been a steady increase averaging about 1.1 percent annually over the last 10 years. Because this increase is long-term and steady, it can be expected to continue. The increase in milk production per cow will satisfy about half of the increase in butterfat needed to meet demand as calculated by the USDA based on Butterfat.

The increase in production of milk per cow is an important factor in financial management of dairy farms. If the same amount of milk can be produced by fewer cows, this creates a very significant opportunity for cost reduction.

|

| Chart III - Milk per Cow |

There is one more element in the supply of milk needed to meet demand. That is the level of components in the milk. As mentioned in the last post, the demand for milk is increasingly centered around components, not milk volume. With fluid milk consumption decreasing and cheese and butter increasing, the level of components in milk are an important element in meeting the demand for dairy products.

Chart IV shows the increase in percent butterfat over the last three years. The average component level of butterfat has increased by .8 percent per year. The combination of increased butterfat per pound of milk and the increase in milk production per cow amount to an increase in butterfat of two percent per year, matching the overall domestic consumption for butterfat with NO additional cows. In fact, to be in balance, fewer cows may be needed.

The expansion of herd size for efficient producers will likely continue. But it will have to be offset with less efficient herds shutting down. This has lead to the trend of fewer producers as smaller herds are often less productive than large well managed herds.

During the time of high butterfat prices, the increase in butterfat levels averaged a growth of 1.2 percent annually. This period covers butterfat from the start of 2018 to September 2019. This shows what is possible in increasing butterfat levels. If the 1.2 percent increase in component levels was maintained, fewer cows would be needed than exist today.

|

| Chart IV - Percent Butterfat in Milk |

Chart V is perhaps the most important chart in this post. It is the only chart which does not show a steady increase in productivity. The spread between the low and high levels of protein production is very small, only .03 percent. The difference between January 2018 and May 2020 is essentially "no change". During the time of significant growth, milk protein levels increased by .6 percent annually. This occurred between mid 2018 and mid 2019. Milk protein is needed for efficient cheese making and it is typically the highest paying component.

|

| Chart V - Percent Milk Protein in Milk |

The fact that butterfat levels quit growing in September 2019 is likely linked to the drop in milk protein levels which occurred during the same time. When diets are formulated to increase milk protein, they will also increase butterfat. The milk protein component levels are manageable and are an opportunity. There is a tendency to reduce amino acid balancing when milk protein price levels are low. However, with all things considered, protein production, butterfat production, health factors, and other benefits, it always pays to balance amino acids. The Milkpay app for quantifying economics can be a helpful tool.