Producer milk prices for all four Classes of milk are based on the commodity prices of cheese, butter, dry whey, and nonfat dry milk. Class III milk (the largest use of milk) is priced based on cheese, butter, and dry whey. Cheese is by far the most important commodity in pricing Class III milk. This post will cover where cheese and butter prices are going.

The formulas for butterfat, milk protein, and Class III milk are tightly linked to the USDA cheese and butter prices. These formulas are shown below in their simplified form. These formulas apply to the producers paid on the Class and Component system which makes up most of the milk in the Federal Orders. Those paid on the Advanced system do not get paid for protein specifically, so their pricing is based on skim milk and butterfat only.

Butterfat = 1.2 x Butter Price - .21

Milk Protein = 3.2 x Cheese Price - 1.3 x Butter Price - 4.43

Class III Milk = 9.6 x Cheese Price + 5.9 x Dry Whey Price + 0.4 x Butter Price - $3.20

Butterfat pricing is based strictly on the wholesale price of butter. The formula for milk protein is more complicated. In that formula, the price of both cheese and butter are used to price milk protein. They are configured such that when the price of butter gets higher, the price of milk protein goes down. So, with higher butter prices, the value of butterfat goes up and the price of milk protein goes down. That is why the most influential commodity for Class III pricing is cheese. Dry whey has a low value and butter has little impact on the Class III price. The cheese price used in the milk protein and Class III formulas above is calculated based on the wholesale price of Cheddar cheese.

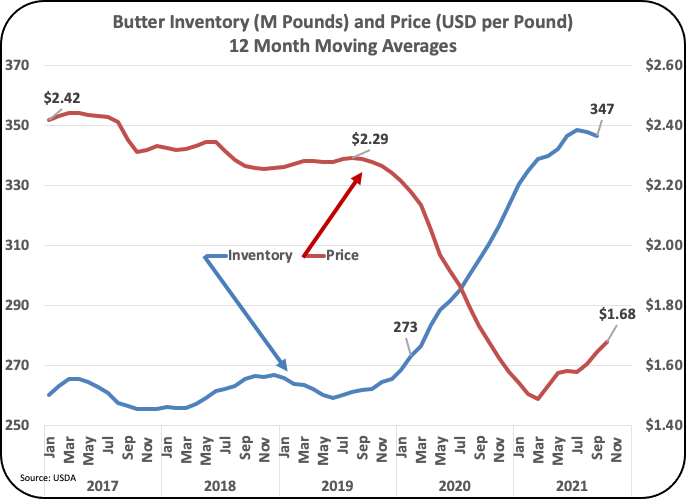

Butterfat pricing will be covered first because it is the easiest to explain. Chart I shows the relationship between butter inventories and butter prices. When supplies are scarce, the price is high. When supplies are more plentiful, the price is lower. In 2017 through 2019, butter inventories were low, and prices hit record highs. As inventories increased in 2020 and 2021, the prices fell.

|

| Chart I - Butter Inventories and Pricing |

The supply side for butter is based on butter production (churning) shown in Chart II. Butter production was low in 2019, keeping butter supplies tight. This changed in 2020 and early 2021 and with higher butter production, inventories grew, and prices fell. However, in the third quarter of 2021 butter production dropped significantly causing the lower inventory levels and higher prices shown in Chart I. If lower production continues, it will cause tighter inventories and higher butter prices.

|

| Chart II - Butter Production |

|

| Chart III - Butter Net Exports |

Of all the factors influencing butterfat prices, the production of butter is the most concerning. Butter production has fallen in 2021 from 209 million pounds in January to 143 million pounds in September.

Milk protein pricing is more complicated. The pricing is based on the price of Cheddar cheese, for which wholesale inventories levels are not made public, and butter prices, which lower the value of milk protein when the price of butter increases.

Production of Cheddar cheese is increasing, and Cheddar makes up about 70 percent of American cheese production (Chart IV).

|

| Chart IV - Production of Cheddar Cheese |

Inventories of American cheese have taken a very bumpy ride especially in 2020 as shown in Chart V. This Chart represents American cheese inventories, not just Cheddar cheese, but with Cheddar cheese representing 70 percent of American cheese production, American cheese inventory is a good indicator of Cheddar cheese inventories.

|

| Chart V - American Cheese Inventory |

If American cheese inventories continue to grow, cheese pricing will follow its downward trend.

|

| Chart VI - American cheese Inventory and AMS Pricing |

Net exports of American cheese amount to about 2.5 percent of American cheese production. They have been very stable for the last four years, so export fluctuations are not impacting inventory levels.

|

| Chart VII - American Cheese Net Exports |

SUMMARY

Butter prices are increasing as production of butter is decreasing. Exports are never a factor due to tight supplies and high prices. The decrease in butter production will decrease inventories which will increase prices. This will increase the value of butterfat, decrease the value of milk protein, and have little impact on Class III milk price.

Production of Cheddar cheese has increased. As a result, inventories of American cheese are growing. In turn, this has brought a significant decrease in Cheddar cheese prices. Unless this changes, look for lower AMS cheese prices which will reduce milk protein values and lower Class III prices.

These trends will continue to be followed through the fourth quarter of 2021 and updated in this blog.

No comments:

Post a Comment