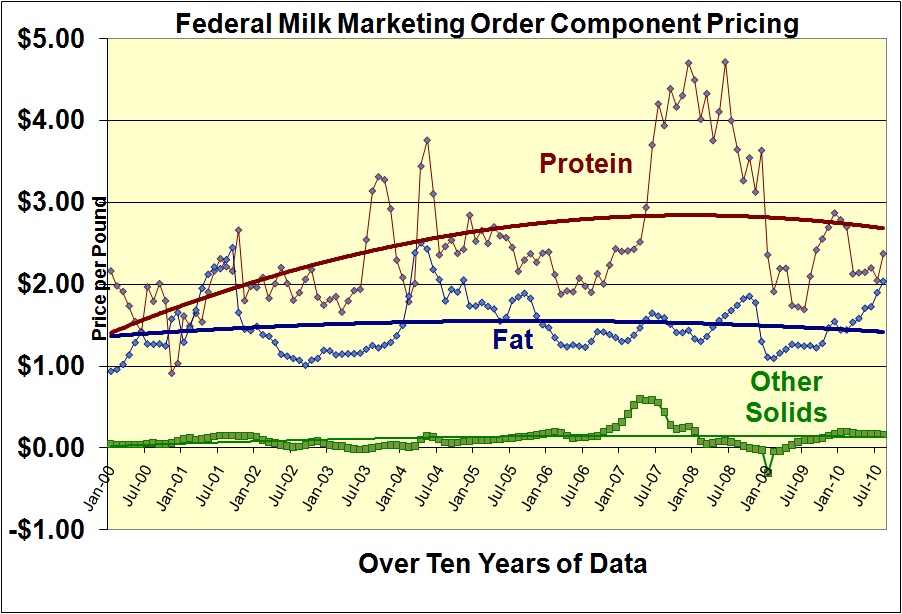

We are in an unusual period in milk component pricing. Butterfat's value is increasing significantly and the price of milk protein is dropping significantly, yet the Class III milk price has barely moved (

see last week's post). This post will examine the math behind this scenario.

The

formulas for milk pricing are available on the USDA web site. We'll examine the simple formulas first.

Butterfat

Butterfat Price = (Butter price – 0.1715) x 1.211

This formula is very straightforward. The butter price is reduced by the cost to make butter (the "make allowance") and then multiplied by the ratio of how much butter can be made from a given quantity of butterfat. The relationship is very direct, as the price of butter goes up, the price of butterfat goes up.

Other Solids

Other Solids = (Dry Whey Price - .1991) x 1.03

The pricing of "other solids" is similarly straightforward. It is based on the dry whey price less the cost to make dry whey multiplied by the amount of dry whey that can be made from "other solids". The only uniqueness to "other solids" is that because whey is very inexpensive, the cost to dry and prepare dry whey can be greater than its market value and when this happens the value of "other solids" become negative.

Milk Protein

Protein = (cheese price - .2003) x 1.383

+ (((cheese price - .2003) x 1.572) - butterfat price x .9) x1.17

The first line of the protein price follows the logic of the "butterfat" and "other solids" formulas. However, the second part shown on the second line above gets more complex both conceptually and mathematically. The second half of the formula gives a value to the increased value of butterfat when it is used in cheese as opposed to butter. This is the part of the formula that can shift the value between butterfat and milk protein without much impact on the overall Class III price.

This relationship will be illustrated in the following graphs.

When the price of butter is constant and the cheese price increases, then the protein price will increase.

However when price of cheese is constant and butter increases in value, the price of protein decreases.

When Cheese goes up within its normal variation and butter decreases in it's normal variation, the price of protein will reach peak values.

When cheese and butter both increase within their normal variations, protein will increase in value, but not as reach high a price as when butter is low.

The Class III prices are really only impacted by cheese prices. We have examined this in

previous posts to this blog. Graphically, this can be visualized as follows.

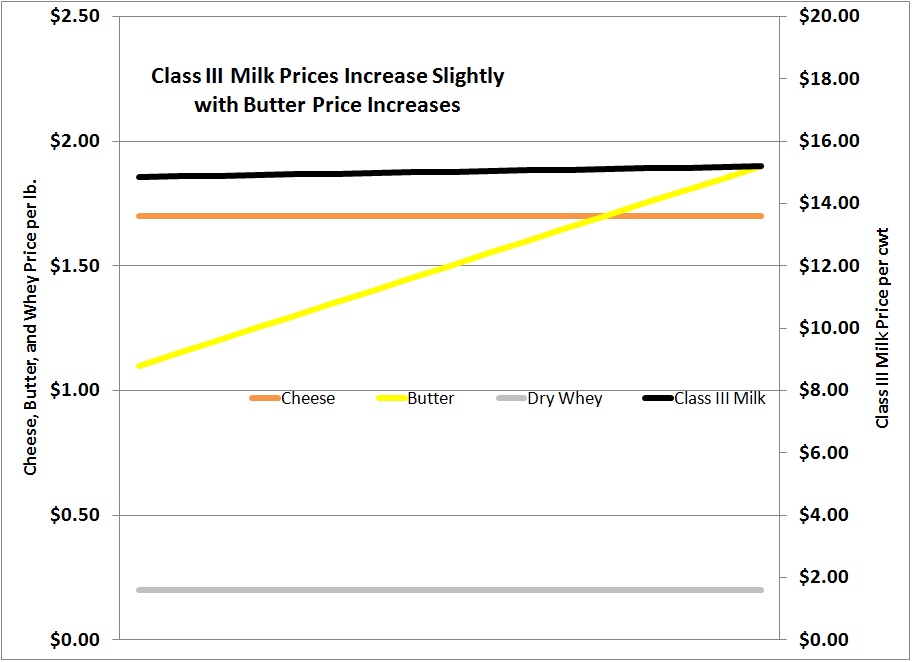

When cheese prices increase significantly, Class III prices increase significantly.

However, when butter prices increase significantly, the class III price barely changes.

When cheese is increasing and butter is decreasing, the Class III price largely ignores the change in butter prices.

When butter and cheese both increase to their historic highs, the Class III price will reach its highest, but that high is close to the high when just cheese prices are high.

In 2010, we have experienced a period where butter prices are significantly up and cheese prices are significantly down. This has created a big shift in the relative values of butterfat and milk protein.

The Class III price has followed only the cheese price.

The chart below shows the two parts of the protein formula separately. While the price of cheese has had only slight variation, the value differential for butterfat in cheese vs. butter has reduced the protein price by nearly $.60.

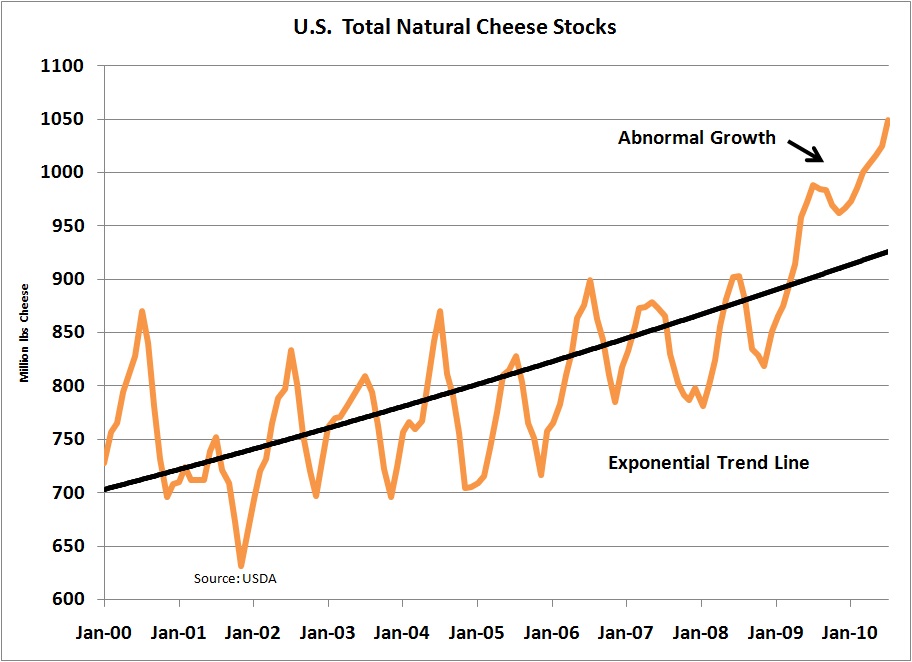

The inventories of butter remain very tight. Therefore, we can probably expect butterfat to command very high prices for the foreseeable future.

The inventories of cheese however are coming more in line with historical levels and we can probably see an increase in Class III prices and the value of protein as this occurs.

{kind=link}