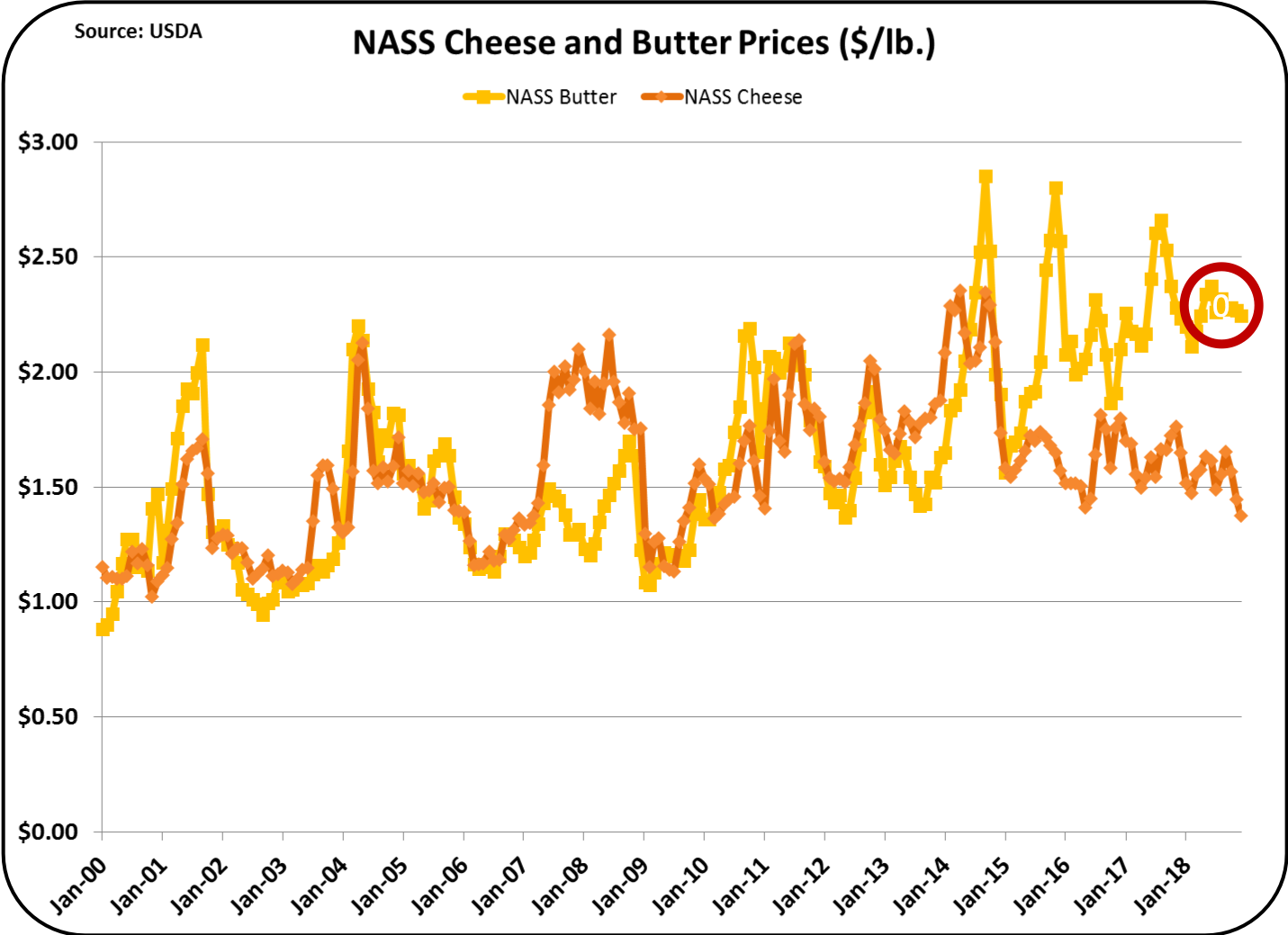

The most

recent Class

III price announcement was made on January 3, 2019 and represents the

Class and Component prices for December, 2018. The price was a

disappointing $13.78/cwt. It was composed of butterfat at

$2.5080/lb., milk protein at $1.1417/lb., and "all other" solids at

$.2775/lb. Calculation of the Class III price is based on skim milk at

3.1 percent protein, and "other solids" at 5.9 percent. That calculates

to a Class III skim price of $5.18/cwt,

Butterfat is

based on a 3.5 percent content in the milk which equals $8.78/cwt. The final

value for Class III is then 96.5 percent skim milk and 3.5 percent butterfat, which

equals $13.78/cwt., the Class III price.

December Class III milk price = $5.18 x .965 + $8.78 = $13.78/

cwt.

The announced

Class III price is only an index. It is always based on milk with the

same component levels, 3.1 percent protein and 5.9 percent "other

solids" in skim milk and 3.5 percent butterfat. That is what an

index is. An index price is based on a constant volume of components that

makes it comparable with all other calculated values for prior months.

However, it

is very rare that a producer supplies milk at exactly these component

levels. A more likely component level would be around 3.8 percent

butterfat, with 3.2 percent milk protein and 5.9 percent "other

solids" in the skim portion of the milk. For that level of

components, the effective Class III price would be $14.64/cwt., That price is $.86/cwt. or 8 percent higher

than the published Class III index price.

Example Class III Price with higher component levels

= (3.2 x $1.1417 + 5.9 x $.2775) x ,965 + 3.8 x $2.5080 =

$14.64/cwt.

The standards

used for the Class III milk price index were developed prior to January 1,

2000, when the current payment system was implemented. The

standards in the Class III index were probably reasonable standards at that

time. Because changing an index price makes it inconsistent with past statistics,

an index is kept at standardized levels.

Increased

component levels can increase producer revenue. Further improvements in

component levels can be achieved. While $14.64/cwt. is not a sustainable

price for most dairy production, it is certainly better than $13.78/cwt. With

just an additional 1 percent increase in protein and butterfat, the milk in

this example would be worth $15/cwt.

Clearly, all

effort to increase component levels for butterfat and milk protein can help

improve dairy profitability. Technology

is available to achieve higher levels of butterfat and milk protein. Implementation is being achieved in many

herds today.

The majority of dairy products require only components. Measurement of dairy productivity by pounds

of milk is not an effective measurement.

The important statistic is component levels. The current growth products like cheese and

butter require only components.