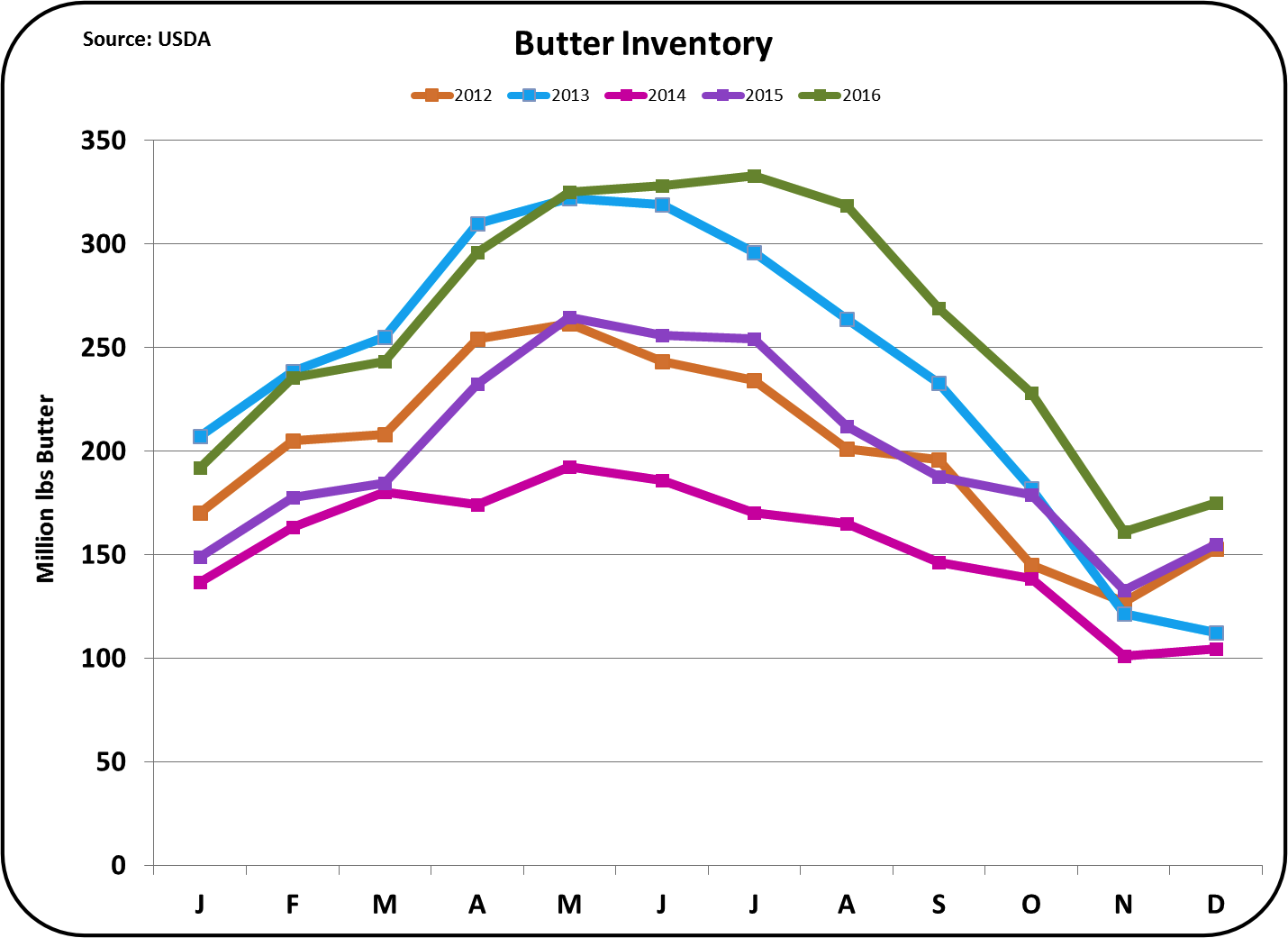

Butter exports remained extremely low as U.S. prices for butter were well above international prices for most of 2016. Increased consumer demand for butter in the U.S. combined with lower U.S. production has kept U.S. stocks low and prices high.

The little butter that is exported is primarily going to Canada and Mexico (see chart below). Canada has a very protective dairy industry, which does not allow any imports except for a few specialty products. The Canadian dairy import market is protected by exclusion from NAFTA and trade agreements with other countries. So why is Canada our largest butter export market? The Canadian dairy industry is isolated with almost no exports and tight restrictions on imports. The payment system is very favorable for Canadian dairy producers, but this results in higher wholesale prices of dairy products. The higher Canadian prices make it difficult for the Canadian dairy market to compete internationally.

Per capita consumption of butter in Canada and population growth have put pressure on butter availability. When butterfat is removed from milk the resulting skimmed milk or skimmed milk powder has a very limited market outside of Canada. Because Canada has good transportation and available refrigeration, there is very little consumer demand for skimmed milk powder in Canada. The only solution for excess skimmed milk is to dispose of it. Because dumping skimmed milk is not economically attractive, this is rarely done. Therefore, limited amounts of butter are allowed to be imported into Canada. The U.S. is the closest source.

As Canada enters into world markets with more trade agreements, some of the barriers to dairy imports will be weakened. The possible renegotiation of NAFTA could also have an impact. Because U.S. butter is higher priced, the U.S. butter market may have to compete with lower international prices in future sales to Canada.

Mexico is the second largest buyer of U.S. butter. As will be shown below, they are also the second largest seller of butter to the U.S.

The low level of butter exports has continued for the last two years. For the prior years 2007 to 2014, exports were much more robust as U.S. butter was priced at international market prices.

Imports of butter have remained in a tight range for the last 10 months of 2016, continuing at the 2015 levels. The only real difference between 2015 and 2016 is that 2015 started off with low exports following huge imports in December 2014. From March to December, 2015 and 2016 were exports were closely matched.

Butter imports are coming mostly from three countries, Ireland, Mexico, and New Zealand. Why is so much butter going back and forth across the U.S./Mexico border? Butter in Mexico is less expensive than in the U.S. Butter is a relatively high cost product in Mexico diets, so vegetable oils are often used in place of butter, keeping butter consumption lower. Butter can also be imported into Mexico from other countries at low international prices. Therefore, the best Mexican strategy is often to export Mexican butter to the U.S. which is allowed via the NAFTA program.

There is now a four year trend of increased butter imports to the U.S. While they have not reached the record levels of 2004 and 2005, if these trends continue, new record imports could occur.

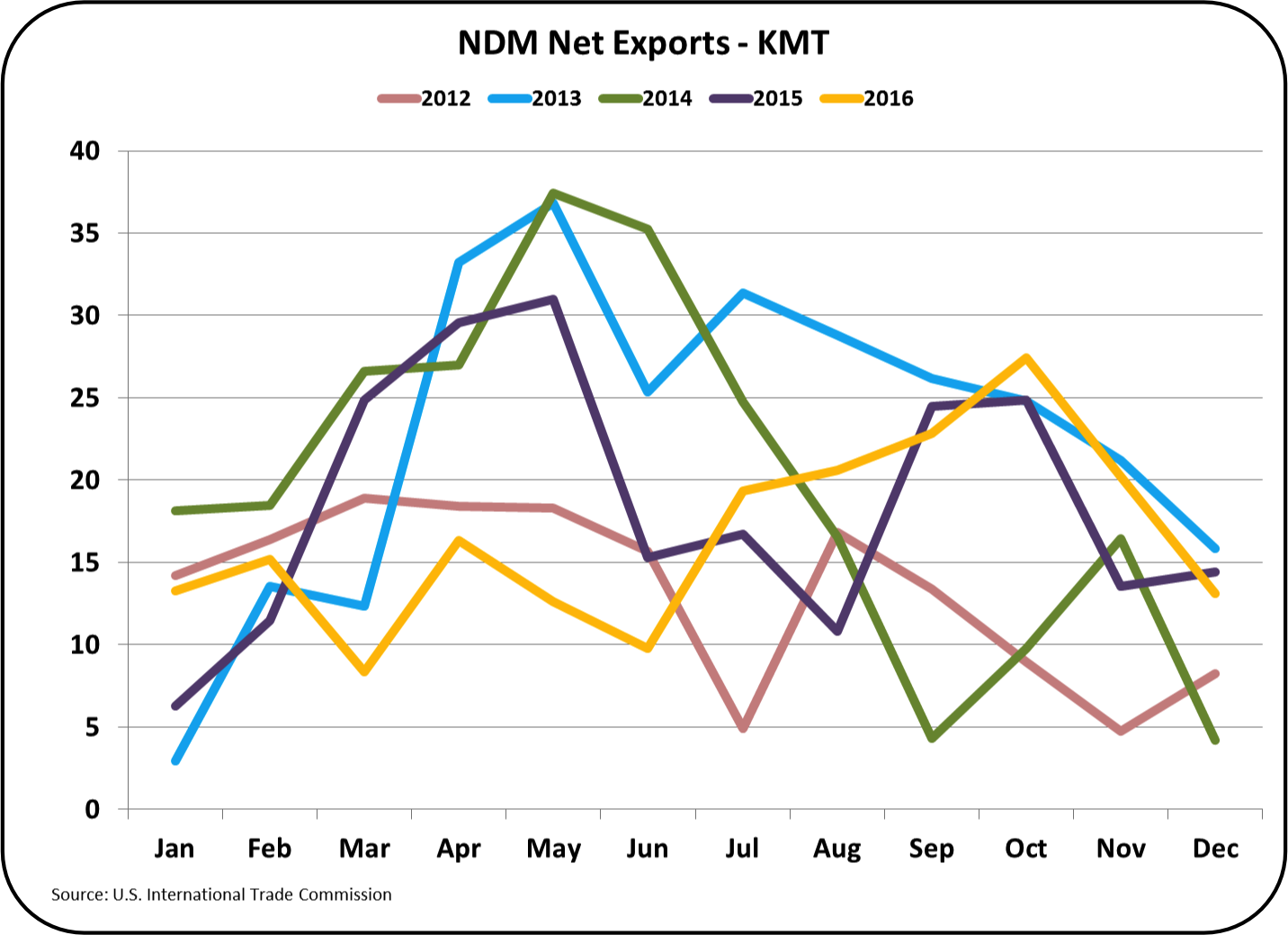

As a result, net exports of butter remain negative, meaning that the U.S. is a net butter importer. The net imports expanded in 2016, not so much a result of exports which increased slightly, but because imports increased more than exports.

This allowed the U.S. to squeak out a record setting volume of NDM exports in 2016.

However, prices were half of the prices received in 2014. The U.S. has remained aggressive in NDM pricing competing successfully against the EU and New Zealand.

Imports of NDM have been at or near record levels for every month in 2016. The main suppliers of NDM to the U.S. are New Zealand and Canada. The reason for the high level of NDM imports from Canada was covered above. New Zealand imports were based on favorable pricing.

Overall, net exports of NDM were below prior years. The increased levels of exports at the end of 2016 were outmatched by the increased levels of imports. While record levels of exports were "squeaked out," record levels of imports hit strong record levels.

This did result in the fourth straight year of declines in the net exports of NDM. Since 2013, net exports of NDM have declined in volume by more than 25%.

If TPP had been approved, all protection from imports including the two-tiered tariff and quota program would have been eliminated (see prior post). With a strong USD and global overproduction, imports might have increased well above the 2016 levels.

The dairy export/import market could be volatile in 2017 as new approaches to international trade are discussed and new trade agreements implemented. Those events will continue to be covered in the blog.

{kind=link}

{kind=link}

{kind=link}

{kind=link}