Dairy exports help create demand for dairy products. This post explores the 2022 exports compared to the prior years and compares exports to domestic production for the four commodities used to price producer milk: cheese, butter, nonfat dry milk (NDM), and dry whey.

Tables I & II put a perspective on the size of these exports. The largest export volume of these commodities is NDM/skimmed milk powder (SMP) followed by dry whey. These are really the byproducts of butter and cheese production. The export of cheese and butter are much smaller than their byproducts. Exporting NDM/SMP and dry whey do not increase the amount of milk needed from dairy producers, but the export market does provides a way to sell the byproducts at a decent price. Increasing exports of cheese and butter does expand dairy milk production.

|

| Table I - Exports of Key Dairy Products |

Table II compares the exports to domestic production. Butter exports reached 9% of production in 2022 and concluded the year with a positive net exports (exports exceeded imports) which has not been the case in recent history. Cheese exports also grew significantly reaching 7%.

|

| Table II - Exports Compared to Production |

CHEESE

Cheese exports are doing very well with a 10% growth in 2022 (Chart I). Chart II shows the six largest importing countries. They all increased purchases in 2022 over 2021. Mexico is the largest importer of cheese and Chart III shows their significant growth in 2022. Mexico increased imports by 16% in 2022 over the prior year.

Cheese production is the biggest use of domestic milk. Exports of cheese can have a major impact on growing the U.S dairy industry.

|

| Chart I - U.S. Cheese Exports |

|

| Chart II - Largest Cheese Importing Countries |

|

| Chart III - Cheese Imports to Mexico |

BUTTER

Butter also saw significant growth in exports (Chart IV). Overall, butter exports increased by 44%, a very major accomplishment.

Out of the top five largest importers (Chart V), four saw significant growth in imports. Canada doubled their butter imports in 2022, Mexico quadrupled their imports, Bahrain increased business by 38%, and South Korea more than doubled their imports (Charts VI and VII).

This is also a very positive accomplish, again increasing business for producers and processors.

|

| Chart IV - U.S. Butter Exports |

|

| Chart V - Largest Butter Importing Countries |

|

| Chart VI - Butter Exports to Canada |

|

| Chart VII - Butter Exports to Mexico |

NDM/SMP

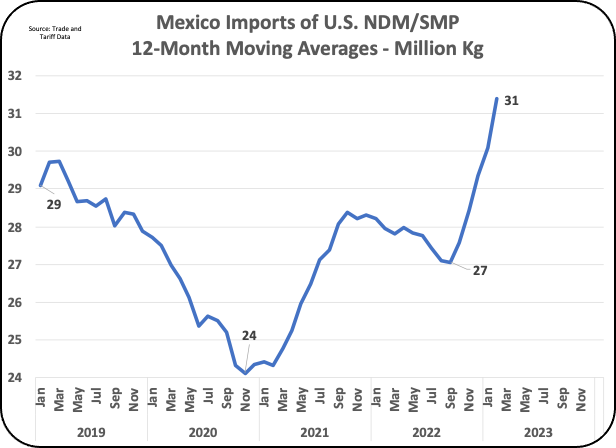

Exports of NDM/SMP declined in 2022 (Chart VIII). Mexico is the largest importer of NDM/SMP and Mexico increased the volume of imports by 7% over the prior year (Chart X). The Philippines, Indonesia, and China finished at volumes close to the prior year (Chart IX). However other buyers like Vietnam dropped U.S. imports by half. As covered in the

prior post, NDM/SMP prices have fallen with heavy competition. With very low international prices and other competitors anxious to sell, the growth of U.S. exports may be slow. In 2022, 73% of NDM/SMP was exported.

NDM/SMP has a good shelf life and is a byproduct of butter churning.

|

Chart VIII - U.S. Exports of NDM/SMP

|

|

| Chart IX - Largest NDM/SMP Importing Countries |

|

| Chart X - NDM/SMP Exports tp Mexico |

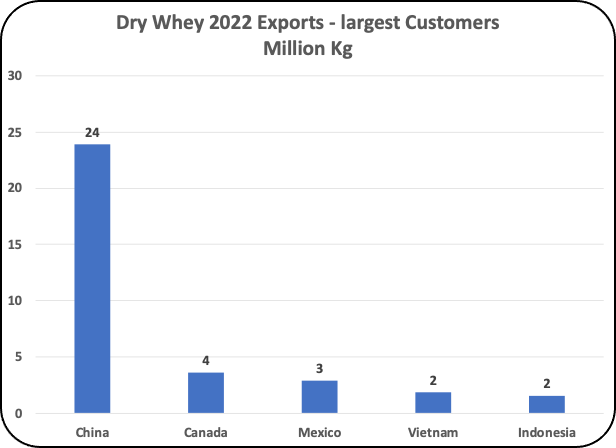

Dry whey export data can be confusing. The USDA definition uses strict limitations for dry whey and does not include modified dry whey products. Other sources include modified whey like whey permeate (whey with no whey proteins). The market for whey permeate is huge in the international markets. It is typically used in feeding swine. Mixing whey permeate with feed for swine can improve eating and weight gain. China is a huge importer of whey permeate. The charts below include regular dry whey and modified dry whey products. The definition used by the USDEC does include modified whey products.

Charts XII and XIII show the huge and growing Chinese market for whey permeate.

|

| Chart XI - U.S. Exports of Dry Whey |

|

| Chart XII - Largest Dry Whey Importing Countries |

|

| Chart XIII - Dry Whey Exports to China |

SUMMARY

The gains in exports of cheese and butter are exciting to build on. Future gains can make exports a major source of demand for U.S. dairy products.

Finding a lucrative home for the NDM and dry whey byproducts can improve dairy revenue. However, selling on the international markets can be volatile and disrupt supply and demand. With that, prices can be volitive.