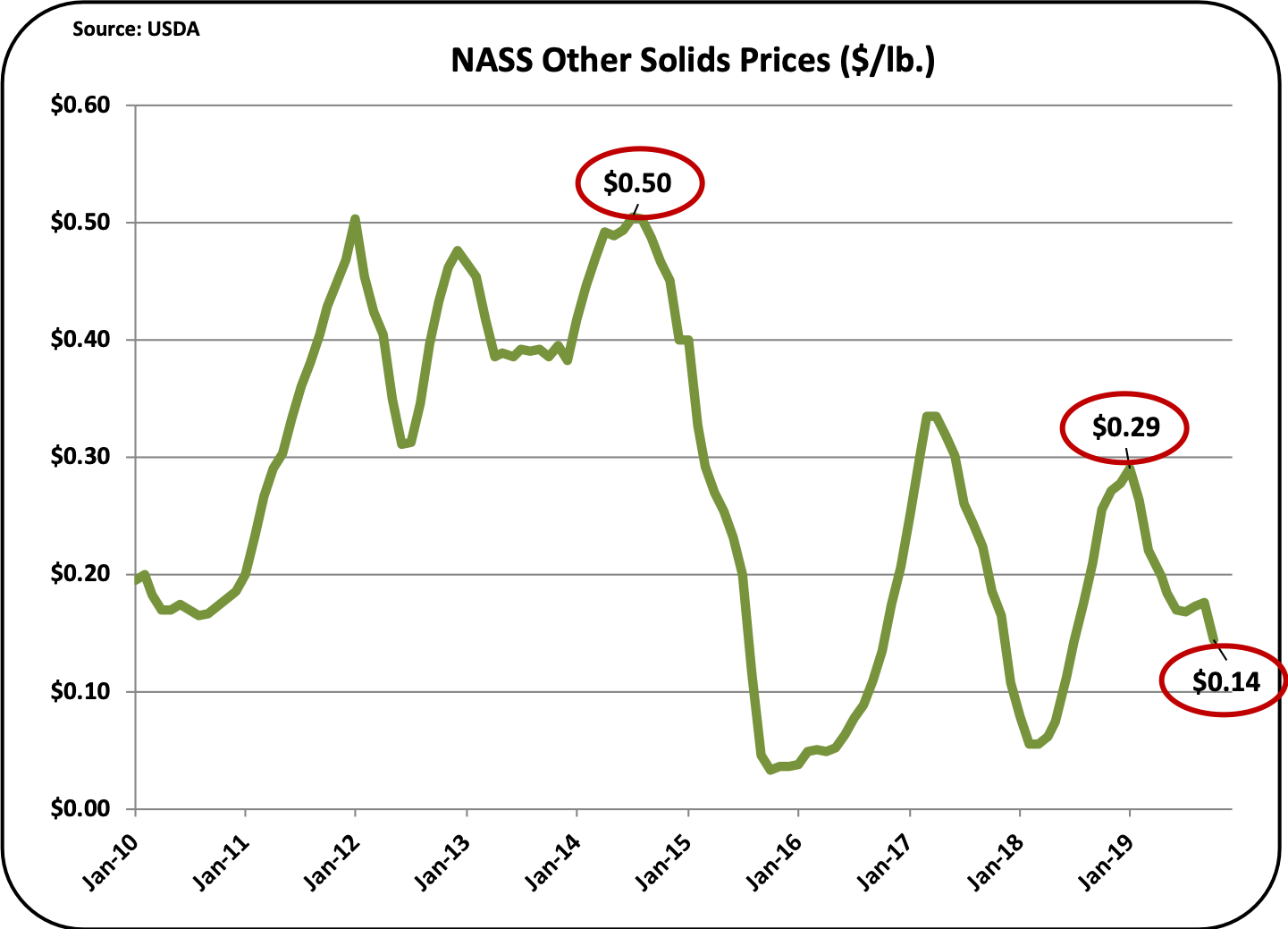

CHEESE

Cheese net exports (exports less imports) are shown cumulatively in Chart I for 2018 and 2019. The two parallel each other very closely. Through the third quarter of 2019, net export volumes of cheese were up by just one percent compared to the prior year.

Cheese exports reduce cheese inventories and cheese imports add to inventories. The two combined as net exports measure the total impact of exports and imports on cheese inventories. A growth of only one percent in net exports is a slower growth rate than domestic cheese production and consumption which are running between a two and three percent annual growth. Therefore, cheese net exports are a shrinking portion of cheese "disappearance."

|

| Chart I - Net Exports of Cheese |

|

| Chart II - Cheese Exports |

|

| Chart III - largest Cheese Export Markets |

|

| Chart IV - Imports of Cheese |

|

| Chart V - largest Cheese Import Markets |

Butter net exports have declined significantly in 2019 compared to 2018 (Chart VI). Net exports had fallen to negative numbers in late 2018 and that decline in net esports is now increasing. That means that the U.S. is a net importer of butter. The negative net exports increased from four million pounds of butter to 26 million pounds of butter in 2019 YTD. The change is the result of both lower exports and a surge in imports.

|

| Chart VI - Butter Net Exports |

|

| Chart VII - Butter Exports |

Butter exports to the two largest butter export markets, Canada and Mexico, fell sharply in 2019 (Chart VII). Exports to Mexico dropped by 72 percent, and exports to Canada dropped by 41 percent. Butter exports to other countries were small.

|

| Chart VIII - Butter Exports by Country |

|

| Chart IX - Butter Imports |

Imports of "Irish" butter are up 27 percent from the prior year and YTD make up 44 percent of all butter imports. The consumer demand for this cultured butter is strong and growing very fast. It is impossible to brand a competitive U.S. product, because the product is typically branded as "Irish" butter with names like "Kerrygold". While consumer consumption of butter is growing nicely, nearly half of the growth is in imported "Irish" butter. That reduces the demand for production of domestic butter.

The hope of all dairy producers is that exports will expand to keep pace with milk production expansion. That would solve the problem of milk over-production which causes increased inventories primarily of cheese. Large inventories of cheese decrease cheese prices and in turn decrease the Class III milk price.

However, the increase in cheese exports remains anemic and an expanded cheese export market is not happening! Cheese net export increases of just one percent will not soak up excess milk that results from over-production and falling dairy consumer demand.

Increased production of butter for export would also increase the production of nonfat dry milk (NDM). NDM is primarily an export item and the international market for NDM is crowded. As a result, there are limited increases in butter churning.

Perhaps with approval of the new trade agreements like USMCA, there will be increased growth of U.S. dairy exports. As of this date, those approvals seem to be held up by political squabbles.