On October 2 the Federal Milk Marketing Order Class and Component Prices for September were announced. Due to the Federal Government shutdown, the website usually referenced here is not available. In place of that document, the Upper Midwest announcement is referenced. The Class III milk price of $18.14 was improved by $.23/cwt. from the prior month.

Every component tracked on the monthly dashboard below was positive. Additionally, the high inventories of cheese that were mentioned in prior posts to this blog have been reduced. As a result, Class III future prices have also improved.

The September prices follow the long-term trends at reasonable levels. Protein increased to $3.54/lb. and butterfat increased one cent to $1.52/lb. Other Solids, steady at $.39/lb. continue to contribute over $3/cwt. to the Class III milk price.

The breakdown of the Class III milk price again set a record for protein, with protein making up 59% of the Class III price. Butterfat's contribution fell to 29%.

Very importantly, the high inventory levels of Cheese seen in the first half of 2013 have drastically improved. Increased exports started to materialize in July 2013. No later data is available, but it is extremely likely that when the data is reported, it will show a continuation of this trend.

This month's data is extremely positive. Therefore, the remainder of this post will deal with a new trend that is having an impact on milk pricing. Nonfat Dry Milk exports are very robust and they have led to a 13% increase in the price of Nonfat Dry Milk. The impact of this change is disproportional within the Federal Milk Orders as will be analyzed below.

THE IMPACT OF NONFAT DRY MILK PRICING

The price of Class III milk is determined by the NASS cheese price (see the April 23, 2009 post to this blog.) However, the price of Class IV milk is determined by the price of Nonfat Dry Milk. The price of Class IV milk can influence the price of Classes I and II Milk and can also impact the Producer Price differential. The winners in this scenario are the Federal Orders paid on the Advanced System and the Orders paid on components that produce significant amounts of Class I, II, and IV milk.

The Class I price is announced in Advance of the month. The price of Class I Skim Milk is based on the higher of the Advanced Class III or IV Skim Milk Pricing. The majority of the time, the Advanced Class III is the higher. However, this changed starting in March 2013.

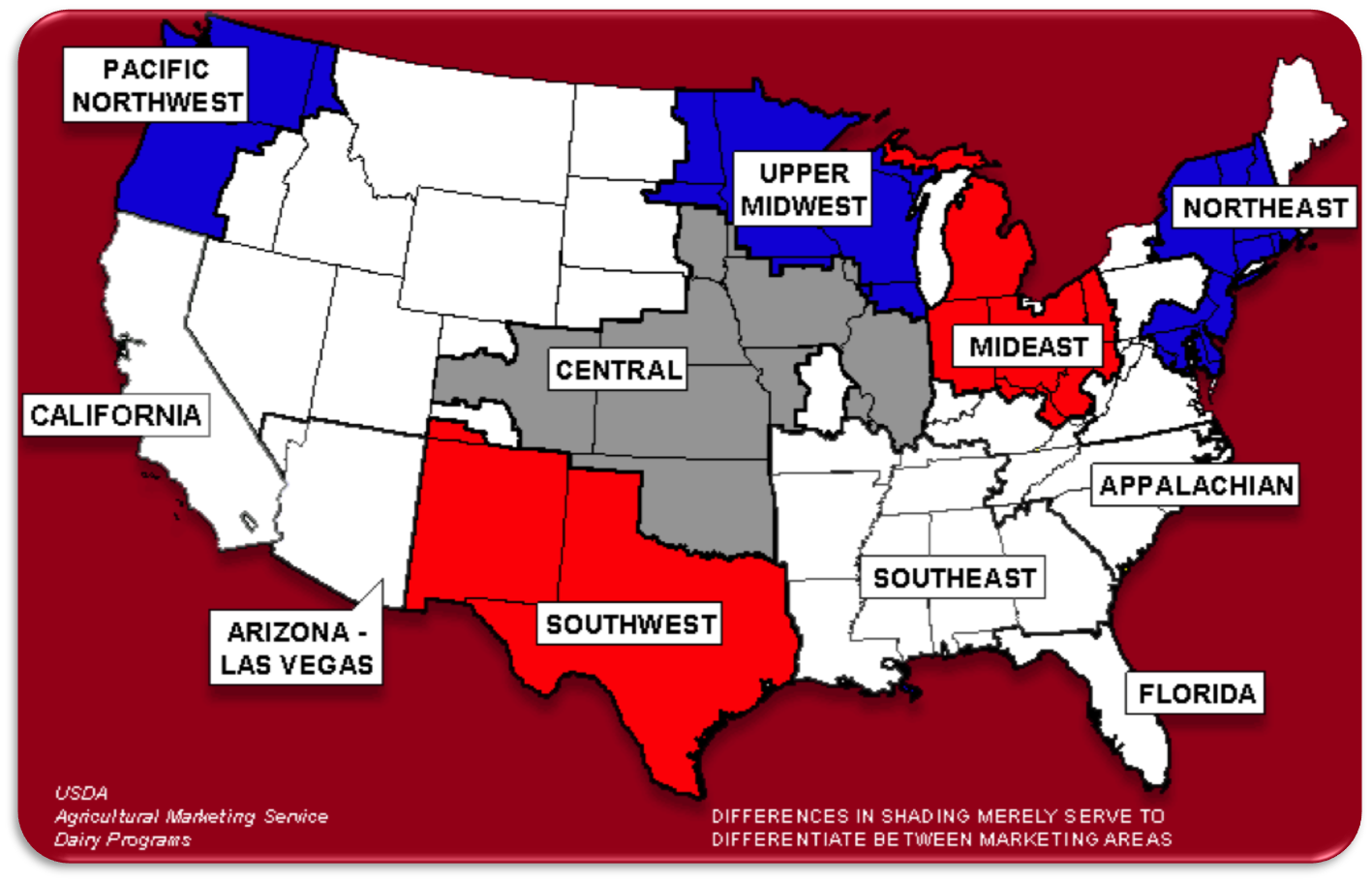

By October, the differential between the advanced Class III and IV was $1.33/cwt., a clear advantage for Class I milk pricing. Who does this impact the most? The four Federal Orders paid on the advanced pricing system (about 11% of the USA milk produced), include Florida, Southeast, Appalachian, and Arizona - Las Vegas Federal Milk Orders. These Orders get the advantage of the higher Class I price. Arizona - Las Vegas also has the benefit of having a significant Class IV NDM business, produced primarily for export.

This price increase for Class IV milk was driven by increased exports of NDM, illustrated in the chart below.

Nonfat Dry Milk exports were up 16% YTD for the first seven months of 2013 vs. 2012. YTD 52% of the NDM/SMP was exported.

This also impacts the Producer Price Differential of the Six Federal orders paid on components (see the May 10, 2009 post for a more detailed explanation of the Producer Price differential). Producers in these six orders are initially paid at the Class III price. The difference between the Class III milk price and the weighted average of the four milk classes is the Producer Price Dfferential.

In 2012, the percentage of each of these classes was a follows:

The Federal Order with the least amount of Class I, II, and IV has the least advantage. This characterizes the huge Upper Midwest Order where 79% of the milk is Class III for cheese production. The Northeast Federal Order has the biggest gain with 78% of its milk in Class I, II, and III. The Producer Price Differentials for August were announced in mid-September and are as follows.

The interrelationships in these calculations are complex. Please feel free to contact the author with any questions.