This post will review the changes in producer milk prices since the introduction of the current Class and Component pricing system which was introduced in January 2000. After nearly 22 years, what way are producer milk prices moving? All charts in this post are based on 12 month moving averages. Since 2000, inflation has increased by 50 percent. Have dairy prices increased the same?

AN OVERVIEW

Table I shows the five-year average prices of the commodities used to price producer milk. The years 2010 to 2015 produced excellent prices for all four commodities. It could be described as the "golden years" for milk pricing. During the five years from 2015 to 2020, butter increased to extremely high prices averaging $2.45 per pound. In turn this drove down the price of milk protein. (See the

prior post for an explanation of why this occurs.).

In the last 20 months, milk protein has recovered to new price highs averaging $3.36 per pound. Producing maximum protein is a strong revenue generator for those paid on the Class and Component system.

Currently dairy prices are all falling from their highs except for milk protein.

|

| Table I - Five Year Average Prices of Dairy Commodities |

The long-term trends shown in Chart I explain some of the reason for low and negative Producer Price differentials. The Class I prices in Chart I are the Base Class I skim prices. In 2000 when the payment system was implemented, Class III skim milk (the blue line) was the lowest paid. Therefore, the initial payment was well under the average price and Producer Price Differentials (PPDs) were positive. Currently, Class III skim milk is the highest paid. Class IV skim milk was high in the early years, but now is the lowest paid milk. To review the changing PPDs. click on this link.

The clear conclusion from this is that the system developed in the late 1900s and implemented in January 2000 has not changed much. Does it need a complete revision? See some thoughts on this in a prior post to this blog.

|

| Chart I - 22 Year Trends |

- First to be reviewed with be the pricing trends of the commodities that are surveyed by the Agricultural Marketing Service. These include cheese, butter, dry whey, and nonfat dry milk (NDM).

- In turn, how have these commodities influenced the values of milk protein, butterfat, other solids and the skim price of Class IV milk.

- The final charts will review the long-term trends of Class I, III, and IV milk prices

COMMODITIES USED TO PRICE MILK

Cheese prices have averaged $1.59 per pound over the full span of nearly 22 years. The current 12-month average is $1.78 per pound. Cheese prices increased steadily is the first decade of the current Federal Order pricing, but in the last ten years, the price of cheese has been stagnant. While there have been swings in the pricing, over the last 10 years, the price has averaged $1.75 per pound. Current cheese prices at $1.78 per pound are right at the 10-year average price.

However, since 2000, the first year of the current pricing system, cheese prices have increase by 58 percent in line with inflation. Most of these increases occurred in the first 15 years of the current Class and Component pricing system.

|

| Chart and Table III - Cheese Pricing |

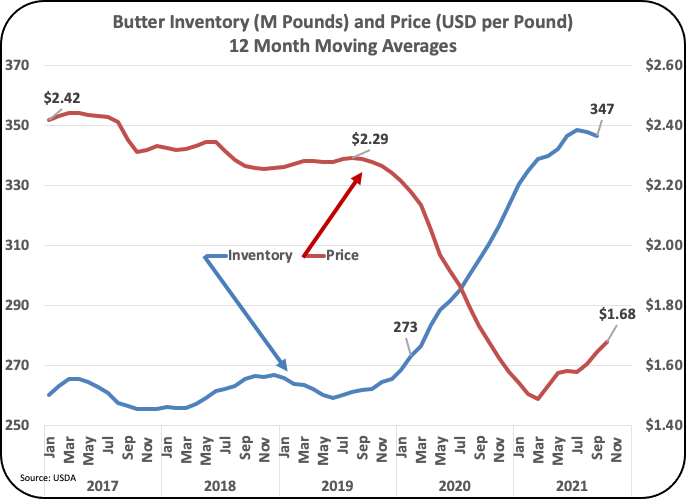

Butter prices have risen significantly through 2019. Over the full span from 2000 to the present, butter has averaged $1.67 per pound. The last 12 months have averaged $1.59 per pound. During the last 10 years, butter prices were at historical highs, averaging $1.96 per pound. From the year 2000, butter prices have increased only 38 percent, well below inflation for this time span.

|

| Chart and Table IV - Butter Pricing |

Dry whey which is used to price "Other Solids" in the component system averaged $.37 per pound over the entire 22-year span. The price for the last 12 months has risen to $.51 per pound, slightly above the last 10-year average of $.46 per pound. In 2000, dry whey was worth almost nothing, averaging just $.19 per pound. The increase to the current price of $.51 per pound represents a 168 percent increase compared to the 2000 price.

|

| Chart and Table V - Dry Whey Pricing |

VALUE OF MILK PROTEIN, BUTTERFAT, OTHER SOLIDS, AND NDM

These above commodities are used to price milk protein, butterfat, and other solids. The price of milk protein has taken a a rollercoaster ride. Milk protein is based on the value of cheese and butter. When cheese prices go up, milk protein goes up in value. When butterfat prices go up, the price of milk protein goes down. See this

past post for a review of the formulas.

Milk protein has averaged $2.59 per pound over 22 years. The last 12 months have averaged $3.27 per pound. In the last decade, when butter prices were high and cheese prices were relatively low, protein was worth $2.72 per pound. Comparing the last 12 months to the year 2000, the price of milk protein has increased by 93 percent, well in excess of inflation.

|

| Chart and Table VI - Milk Protein Pricing |

Butterfat pricing had a very strong run from 2014 to 2019 (Chart I.) Butterfat is priced based only on the price of butter. Over the last 12 months, butterfat prices has averaged $1.72 per pound, which is a 38 percent increase over the 22 year span of this analysis. This is less than the inflation rate of 50 percent. Over the full span of 23 years, butterfat has averaged is $1.84 per pound, more than the last 12 months average of $1.72 per pound.

|

| Chart and Table VII - Butterfat Pricing |

"Other Solids" pricing is based on the value of dry whey which has been very erratic over the full term of this analysis. Over nearly 22 years "Other Solids" have averaged just $.20 per pound. In 2008 and 2009, the value of dry whey was negative, meaning that it cost more to dry the whey than what it was worth after it was dried. Dry whey is now primarily an export product, and it has gained in value. For the last 12 months, the "Other Solids" prices averaged $.32 per pound contributing nicely to the Class III price. That is well above the first year which was just $.05 per pound and well above the inflation rate. Clearly, new uses have been found for dry whey.

|

| Chart and Table VIII - Other Solids Pricing |

NDM pricing has been erratic at times, but on the average, it is very stable over the long run. NDM prices have increased by only 14 percent in the 22 years of the current Federal Order payment system. Current prices of $1.15 per pound are just slightly above the full-term price of $1.11 per pound.

|

| Chart and Table IX - NDM Pricing |

MILK PRICES

Class III milk prices has increased by 81 percent over the span of this analysis. Class is not near to the highs of 2015, but are around $18 per cwt. This is higher than the Base Class I price.

|

| Chart and Table XI - Class III Pricing |

Class IV milk is now extremely important to overall producer milk pricing. Class IV milk is growing in volume and Class IV skim is used for pricing Class II and it is also used for half of the pricing for Class I. Class IV skim milk pricing is based solely on the price of NDM. Since 2020, the price has increased by only 22 precent, well below inflation during that time.

The low Class IV price is a real problem for overall pricing in Federal Order areas and especially where NDM is produced in large quantities. Class IV milk is the lowest paid milk. The Federal Orders that are touching the oceans for shipping are the major Federal Orders impacted. This includes California, the Pacific Northwest, the Southwest, and the Northeast Federal Orders.

Class IV milk has increased by only 22 percent over the 22 years of the current payment system.

|

| Chart and Table XII - Class IV Pricing |

Class I prices have increased by 46 percent since 2020, very close to the inflation increase over that time.

In 2019, the formula for pricing Class I skim milk was changed. It now uses an average of the Class III and Class IV skim milk prices. When the new pricing for Class I milk was developed, it does not appear to have considered the growing long-term difference between Class III skim prices which increased 124 percent over the last 22 yers and the Class IV skim price which increased by only 8 percent during this time. The difference of $.74 which is included in the new formula is based on historic differences. Due to the extreme difference in price growth rates for Class III vs. Class IV, the historic difference is quickly out-of-date. With this in mind, the longer the current formula exists the lower producer milk prices will go.

|

Chart and Table X - Class I Pricing

|

SUMMARY

Over nearly 22 years, the original Federal Order pricing methodology has led to changes in producer milk prices. In 2007 and 2008 the make allowances were increased three times. When the make allowances are increased, more money goes to the processor and less to the producer. In 2019, the Class I formula was changed to allow for more specific hedgeing by using an average of Class III and Class IV skim prices to determine the Class I skim price. Class I milk volume for drinking is shrinking and Class III volume is growing. NDM has become an export item and the price is now determined by international supply and demand, political events, and currency exchange values. As a result, de-pooling in the Federal Orders has become huge. Is it time for a major change?

In general, producer prices are declining. In 2014 through 2019 butterfat prices were excellent. Now milk protein is showing consistently high prices. To get good revenue, producers paid by the Class and Component system need to maximize production of milk protein and butterfat.