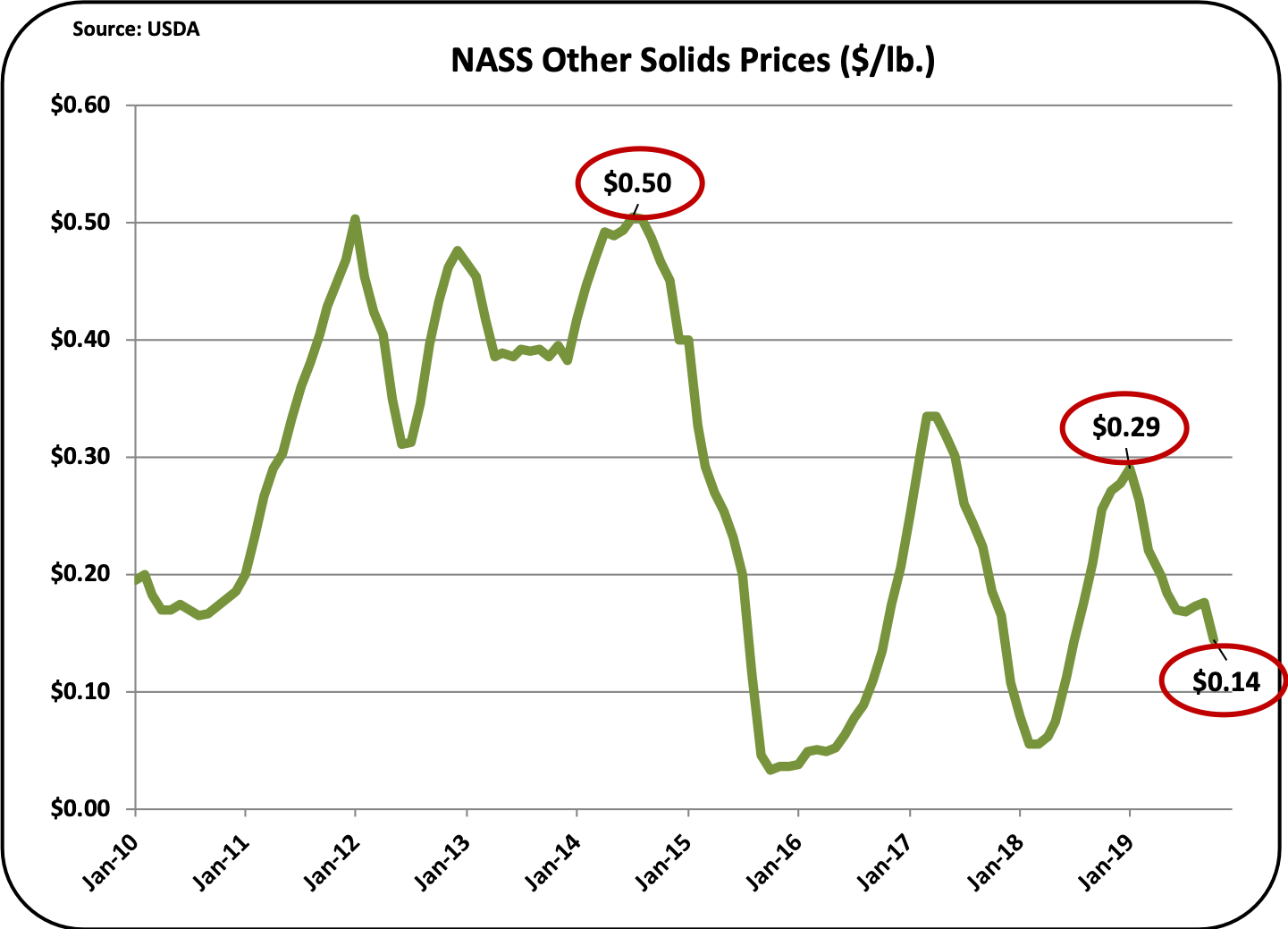

DOMESTIC CHEESE CONSUMPTION

Cheese domestic consumption is the bright spot in consumption of dairy products. The growth rate has slowed somewhat with the maturing of the U.S. cheese market, but it is still growing at a healthy rate.

Chart I shows the growth of per capita consumption of cheese by type of cheese. All types of natural cheeses have increased per capita consumption with the exception of processed cheese products. Since 2000, per capita consumption of natural cheeses has increased from 30 pounds per year to 38 pounds per year. Processed cheese products have decreased from 8 pounds per year to 7 pounds per year. Cheddar and Mozzarella make up 64 percent of the total 2018 natural cheese category. Mozzarella has the biggest share at 33 percent.

|

| Chart I - Per Capita Consumption of Cheese |

|

| Chart II - Makeup of the Cheese Category in 2000 |

|

| Chart III - Makeup of the Cheese Category in 2018 |

Since 2000, natural cheese consumption has increased by 28 percent. Table I below shows the growth by cheese type. The American cheese products other than Cheddar include Colby, Monterey, Jack, and curd cheeses. The Italian cheese products other than Mozzarella include Provolone, Gorgonzola, Ricotta, Asiago, and Parmesan cheese. All the American and Italian "other" cheeses just listed constitute the real movers in the growth of cheese. While they are all relatively small players, altogether they account for 21 percent of total cheese consumed in 2018 and consumption of these cheeses has increased 48 percent since 2000. Swiss, Blue, Muenster, Brick, and others have also seen significant growth.

Mozzarella and Cheddar remain the biggest players. Mozzarella consumption has increased by 34 percent since 2000 and is now the largest individual cheese consumed. Mozzarella has grown with the growth in Italian foods. Cheddar has increased volume by 14 percent since 2000 but now commands only 31 percent share of the current market.

Processed cheese products have decreased by 12 percent during the last 19 years as consumers tend to eat more natural cheese than processed cheeses. Much of the processed cheese uses Cheddar as the base ingredient and have thereby also decreased Cheddar consumption.

|

| Table I - Growth of per Capita Cheese Consumption |

WHOLESALE AND RETAIL CHEESE PRICES

Chart IV shows the wholesale and retail prices of Cheddar cheese since 2000. The dotted lines are trend lines. They are all based on year end prices for each year. The retail price has increased 43 percent over 19 years while the NASS wholesale price has increased by only 27 percent. The spread between the retail price and the wholesale price has increased from $3/lb. to $4/lb. The consumer marketing of cheese has helped grow the retail price. In the last decade, the linkage between the retail and wholesale prices has lost any correlation. As an example, in 2018, the retail price of cheese went up while the wholesale price of cheese went down.

Why is this important? Keep reading. Please note that in 2016 and 2017 the retail Cheddar prices were below the trend line.

|

| Chart IV - Retail and Wholesale price of cheese - $/lb. |

PRICE ELASTICITY OF DEMAND

There is price elasticity of demand for cheese. When cheese is cheaper, more is consumed. When cheese is expensive, less is consumed. In 2016 and 2017, the retail prices were below the trend line and Cheddar cheese consumption was up by 6.6 percent in 2017. In 2018, the retail price of Cheddar cheese rose by eight percent and the Cheddar cheese consumption increased by only one percent, far below the prior year's increases.

|

| Chart V - Cheddar Cheese Price Elasticity of Demand |

With the current higher milk prices, cow numbers and milk production are increasing. However, the growth in cheese production has continued to decline as shown in Chart VI. The data used for Chart VI is not a fleeting month, but a moving 12-month average compared to the prior 12 months. The green line represents the total production of cheese which has slowed to a one percent growth rate in 2019. Cheddar cheese production growth has declined to two percent less than the prior year. All "non-Cheddar" cheese growth is also slowing but is still above a two percent annual growth rate.

The decreasing production is beginning to bring total cheese stocks down. At the end of October, the stocks were down 2.4 percent vs. the prior year. However, that is still a relatively high inventory level of cheese.

|

| Chart VI - 12 Month Average Growth in Cheese Production |

WHAT DOES ALL THIS MEAN?

The rapid increase in milk prices is driven by the blue line in Chart VII. Cheddar production has taken a major dive during 2018 and 2019. In early 2018, the annual growth rate of Cheddar cheese production was near eight percent. In October 2019 it was near a negative two percent growth vs. the prior year. Although data on Cheddar cheese inventories is not publicly available, changes in production obviously drives changes in inventories.

|

| Chart VII - Protein Price vs. Growth in Cheddar Cheese Production |