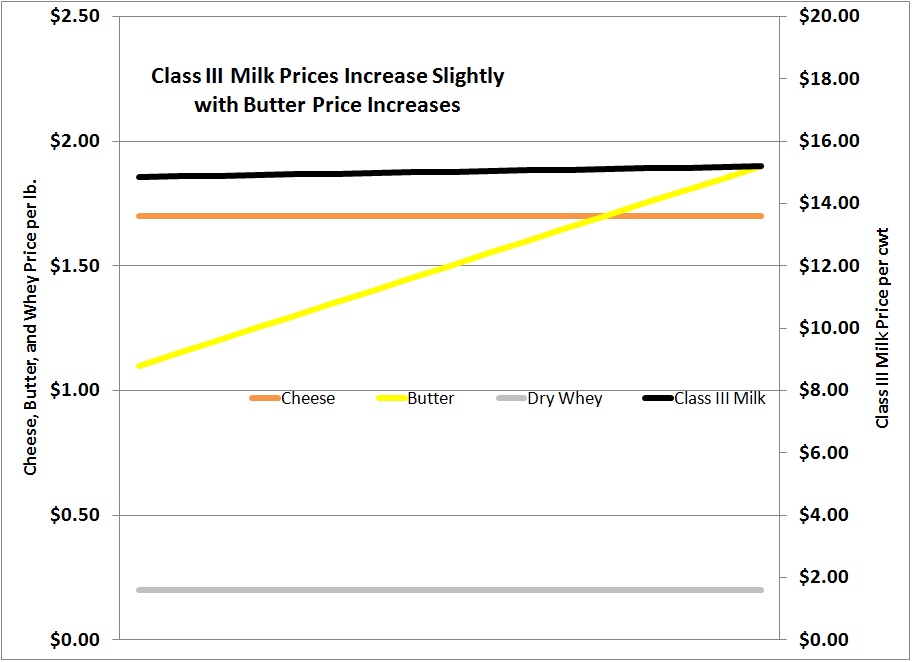

Cheese inventories did not reach their normal seasonal low at the end of 2009. We are now in midyear and the midyear peak appears to be a little high, but not hugely out of line with the growing cheese markets. The annual cycles for American cheese can be viewed on the USDA site.

Butter inventories have been extremely low, with a peak about 50 million pounds below normal levels. A similar situation happened in 2004/5 and butterfat reached over $2.50/lb. The yearly cycles can be viewed on the USDA site.

To better understand what is behind the inventories; below are analyses of imports, exports, net exports (exports minus imports) and production. Cheese statistics will be viewed first and butter statistics second.

Cheese Analysis

Cheese imports are down to the lowest levels in the last 10 years. This should help reduce cheese inventories.

Cheese exports are up significantly, more than tripling the levels of 5 years ago. This should help reduce cheese inventories.

When exports and imports are combined, one can see that the U.S. has gone from being a net importer to being a net exporter. This should help reduce cheese inventories.

Cheese production has remained robust. The annual cycles can be viewed on the USDA site. June cheese production set new high records for this month of the year.

Cheese net exports are healthy, up around 20 million pounds per month. However, cheese production has risen between 20 and 40 million pounds per month. U.S. consumption data is not yet available, but historically it has shown steady and predictable growth over many years. In late 2008 and early 2009, with high milk prices, retail cheese increased enough that demand was suppressed. With lower milk prices, the growth in cheese consumption should be continuing.

Butter Analysis

Butter imports and exports show trends similar to cheese. Less butter is being imported....

...and more butter is being exported, although exports have not reached the heights seen in 2008.

Net butter exports (export minus imports) have reached the point of making the U.S. an exporter of butter.

But while net exports have risen by nearly 10 million tons in 2010, production has not matched this demand. In fact, butter is down approximately 10 million tons. The annual cycles can be viewed at the USDA site.

In summary, the changes in inventories can primarily be linked to production which is out of sync with demand. This will no doubt reverse itself, but for now has created an unusual supply and demand situation that will take months to correct.

{kind=link}