The U.S. economy has recovered faster than the economy of most other countries. Because of this leading economic recovery, the USD, has strengthened vs. other currencies. Unfortunately, this makes U.S. exported items relatively more expensive and less competitive on international markets. Because more than 15% of U.S. dairy solids are exported, a decrease in dairy exports can cause domestic dairy inventories to balloon and force domestic prices down.

The other major international exporters of dairy products are Europe and New Zealand. Because Europe has lost dairy exports to Russia, Europe has been actively seeking other dairy markets. The biggest shift in exchange rates has also been between the USD and the Euro, favoring European dairy product prices on the world markets. As shown below, the USD vs. the Euro has been trending toward a stronger USD for seven years, so this is not a new event. What is new, is the deeper plunge that has occurred in 2014 and early 2015. Since the beginning of 2014, the Euro has fallen over 20% in value vs. the USD.

For European producers and processors, Cheese that sold for $4/lb., could now be priced at just over $3.20/lb. with the same producer and processor profits. European cheeses have an excellent reputation and are strong competitors.

Cheese is not as commoditized as many other dairy products. Butter is pretty much butter no matter who you buy it from, and the same can be said about skimmed milk powder and dry whey. Because much of the exported cheese is sold as branded product, there is also a strong factor of brand loyalty in the international cheese markets. As shown below, exports of U.S. cheese have grown significantly since 2009. However, there is some plateauing in recent months.

The year-by-year charts show a different view of cheese exports. The decline in cheese exports in the last three quarters of 2014 is clear. January 2015 followed this pattern, but February showed a significant reversal. Data for March will be very important, as it will establish whether February was just an aberration or is it the start of a new growth trend.

An analysis of cheese exports reveals the strength and weaknesses of these exports.

Mexico is by far the largest importer of U.S. cheese, representing about 25% of total U.S. cheese exports. These exports appear stable with no deterioration.

South Korea is the second largest importer of U.S. cheeses, representing nearly 20% of U.S cheese exports in 2014. This market also remains solid.

There has been some deterioration in other markets, but overall, cheese exports are stable for the time being. As mentioned in the prior post, there is no significant increase in U.S. cheese inventories.

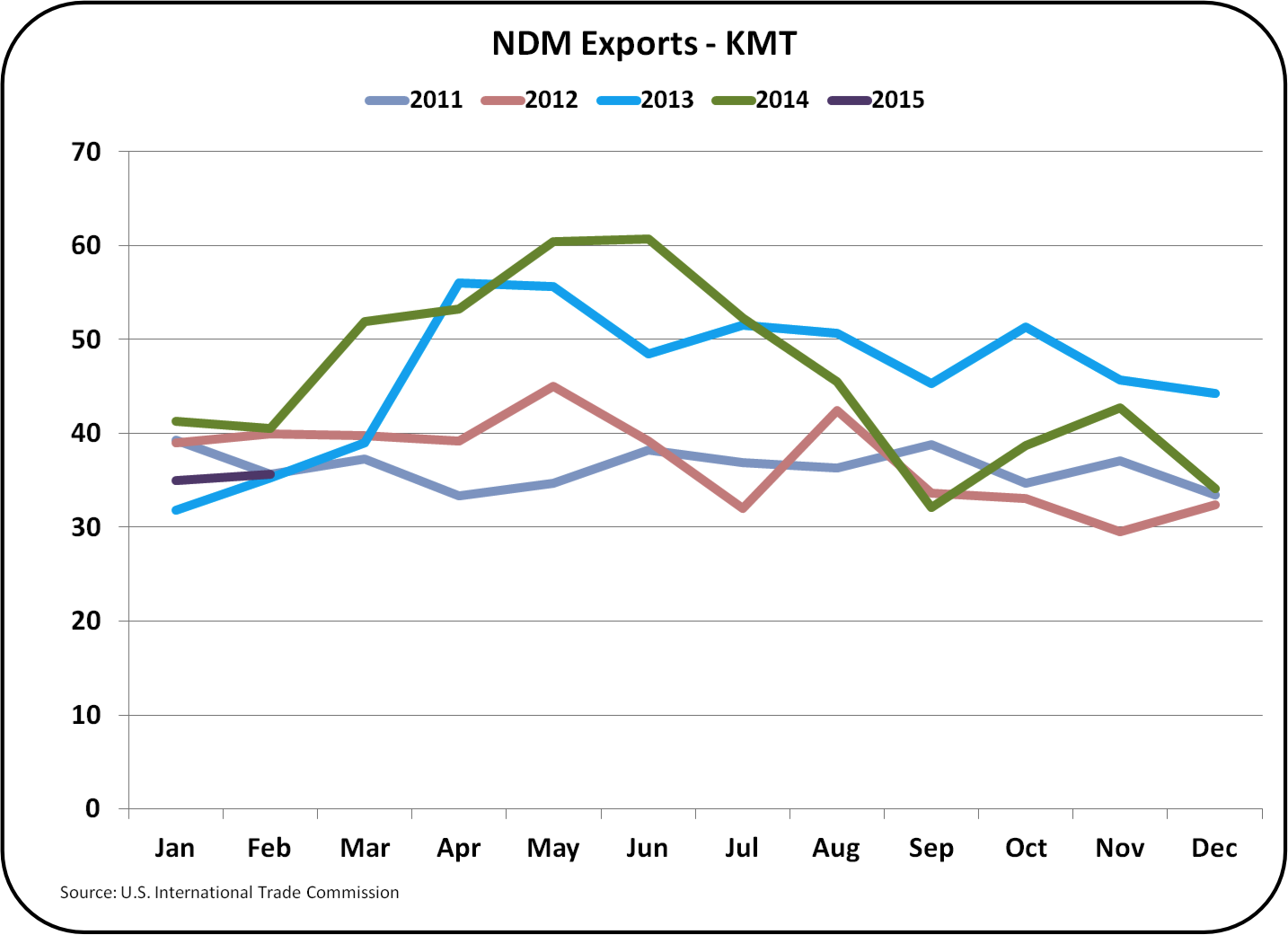

Nonfat Dry Milk/Skimmed Milk Powder (NDM/SMP) is a commodity. The U.S. remains the largest international exporter, but these sales are in jeopardy in term of volume and price.

As the chart below shows, export volume is lower than the prior four years. In the past, Europe has been the largest exporter of this product, and is again making gains in volume growth in the international markets.

Mexico is also the largest importer of U.S. NDM/SMP and historically has consumed 30 to 40% of U.S. export volume. Due to declining sales elsewhere, the stable Mexican imports now account for nearly 50% of U.S. exports. The Asia/Pacific Rim which had grown to be a significant U.S. market has now found better prices and availability elsewhere.

As discussed in the July 16, 2014 post to this blog, NDM/SMP pricing impacts Class IV milk and in turn can impact Class I milk prices.

This international market, which is very much price driven, will cause the U.S. exports of NDM.SMP to underperform until exchange rates shift to a weaker USD.

Exports of whole milk powder, which has been an untapped market for U.S. exports, did grow nicely in 2014. The combination of NDM/SMP and whole milk powder exports did show growth in 2014 over 2013, but the competitive international market still makes it difficult for powdered milk products exports to maintain volume or pricing for the foreseeable future.

Dry whey is the basis for other solids prices, which is one of the three components making up the Class III price. Other solids has been contributing $2/cwt. to the Class III milk price. As shown in the chart below, dry whey exports are at a five year low.

China imported 36% of U.S. exports of dry whey in 2014. This volume has been significantly reduced starting in late 2014, and has fallen faster in the first two months of 2015. Recovery will be difficult.

As shown below, butter exports remain very low. As covered in the prior post, low churning rates have kept inventories tight and wholesales domestic butter prices remain normal.

CONCLUSIONS

The good news on exports is two fold:

1. The important cheese export market remains healthy

2. February exports indicate renewed strength.

The bad news is that the commodity dairy exports are seeing pressure on volume and pricing that will probably persist as long as the USD remains strong vs. the currencies of other dairy exporting countries.