Chart I shows the total volume of fluid milk consumed in the U.S. For many years, the decline in per capita consumption was offset with population growth keeping the total fluid milk consumption relatively stable. However, population growth has slowed, and the per capita consumption of fluid milk has dropped. The growth rate is now negative.

|

| Chart I - Annual Fluid Milk Sales |

|

| Chart II - Growth of U.S. Fluid (Beverage) Milk Consumption |

|

| Chart III - 2017 Milk Volumes by Class |

The makeup of milk is also drastically changing. Turning the calendar back 50 years, whole fat milk was about all there was. Then, as consumers became more calorie conscious, 2% fat milk grew as well as 1% fat milk and skim milk. That trend has reversed in the last five years and butterfat has been shown to have important properties. Butterfat is now recognized to help certain body functions, not just add calories. In 2017, the volume of whole milk was again up over the prior year gaining 2.6%.

|

| Chart IV - Consumption of Whole Fat Milk |

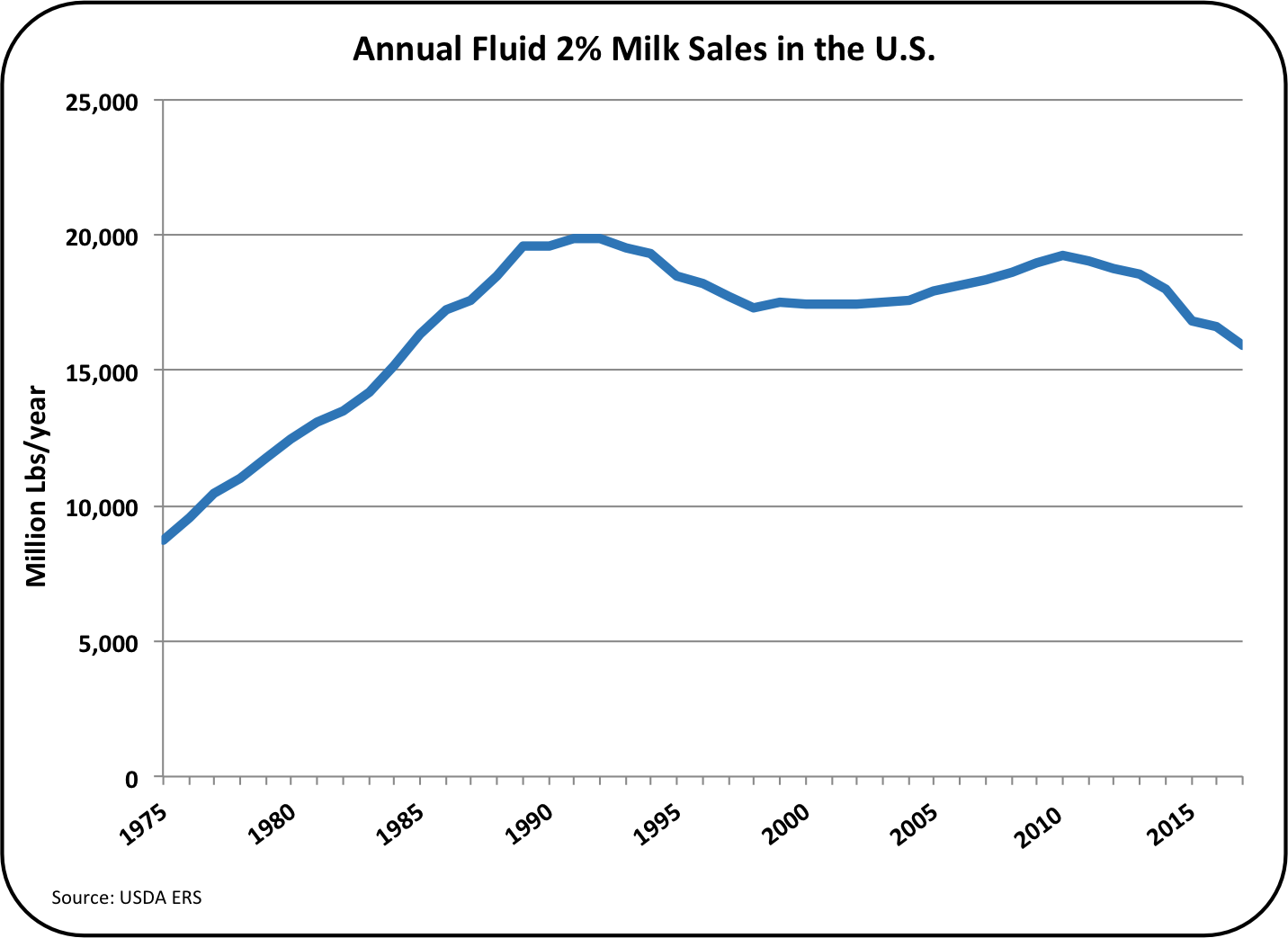

Milk with 2% fat was the most popular milk in 2016. The trends toward whole milk changed that. In 2017, 2% fat milk down 5% in volume. The most popular milk is now whole fat milk

|

| Chart V - Consumption of 2% Fat Milk |

Milk with 1% fat dropped by 9% in volume in 2017. This change follows the overall trend to milk with more butterfat.

|

| Chart VI - Consumption of 1% Fat Milk |

Skim milk continued its drastic fall. In 2017, it fell by 13% from the prior year. Over the last eight years, it has fallen by 48%.

|

| Chart VII - Consumption of Skim Milk |

Adding all the types of milk together, total fluid milk consumption fell 3.3% in 2017 vs. the prior year.

The increased consumption of butter covered in the March 31 post to this blog is only one factor in the overall consumption of butterfat. The changes in consumption of fluid milk with less butterfat being removed has also put pressure on the butterfat supply. In 2017, whole milk made up 34% of the total milk, 4% higher than the prior year.

Where is this trend going? If milk consumption continues to drop by 3.3% per year, fluid milk demand will drop by another 30% over the next 10 years. In the case of fluid milk, export help is minimal as shipping all the water in whole milk very far is cost prohibitive. That would make the demand for Class I fluid milk drop from being the number two category by milk class to number three. Class IV milk which is growing would become the second largest category. States like Florida, where fluid milk consumes nearly all the milk produced, will see a drastic change in the need for milk.

CONCLUSION

The data presented above only confirms what most readers already know. Fluid milk consumption is continuing its slide downward. White milk mustaches appear to be disappearing. The new data suggests that the decline is accelerating. In the statement in the paragraph above, a decline in demand for fluid milk in the next 10 years was estimated to be 30% based on the 2017 decline rate. That may understate the decline which appears to be accelerating. If the declining rate continues to accelerate, as it is now, that decline could be 35% or more over the next 10 years.

When we start to combine the domestic consumption and export trends, it becomes obvious that the productivity standard of measuring pounds of milk production is meaningless. The only thing that is important is pounds of solids, and especially important are pounds of butterfat and protein. While there are many statistics published on pounds of milk produced, there are very limited national or statewide statistics comparing pounds of the various solids produced. The Federal Orders paid on the advanced system will continue to decrease in volume as fluid milk declines. Payment by the component system will continue to grow. Statistics on production of specific solids needs to become the standard measure of productivity.

The most difficult question to answer is how much total milk will be needed. From prior posts, data and trends on population growth, cheese growth, butter growth, and export/import growth were examined. The most volatile of these is exports/imports, because there are many global elements that can influence exports and imports. Current data shows that the milk supply is growing by 1.5% annually. Is there enough demand for all this milk?

In a June post to this blog, the factors mentioned above will be combined to form a model predicting the volume of milk/solids that will be needed going forward.