One of the brightest spots in dairy production is the increase in butterfat. The products like cheese and butter consume most of the U.S. milk. With increased butterfat levels, less milk is needed. Milk production is currently growing at about .5% annually (Chart I). Butterfat production is growing by about 1.5% annually (Chart II). Together, the increases in butterfat availability are growing at about 2% annually. This should provide enough butterfat to satisfy the needs for cheese, butter, and other dairy products (Chart III) without any additional cows.

In round numbers, 60% of butterfat goes to cheese, 20% to butter, and 20% to all other including fluid milk. Butterfat is essential to most all dairy products. Products like nonfat milk and 1% fat milk are declining rapidity (see this recent post).

|

| Chart I - Percent Increase in U.S. Milk Production |

One of the most amazing things is that the growth in butterfat levels, as measured by 12-month moving averages have never been negative in the course of this analysis. The annual growth rate as shown in Chart II ranges from an increase of just .5% to a high of 2.1%. Currently, as of April 2023, the percent growth rate of butterfat is 1.5%. Butterfat production measured in millions of pounds is growing consistently year-by-year (Chart III). In 2017, Federal Order butterfat levels were at 3.8% and currently, they are at 4.1%.

|

| Chart II - Percent Increase in Butterfat by 12-Month Moving Averages |

|

| Chart III - Estimated Butterfat Available from Producers |

Table I below ranks the percent butterfat by Federal Order for April 2023. Federal Orders make up about 60% of total U.S. milk utilization. The overall increase in butterfat levels changed from 4.01% in 2022 to 4.07% in 2023. The Northwest again has the highest butterfat levels at 4.26% with a growth of .25%. All the Federal Orders showed increased butterfat levels in April with one slight exception, the Southwest Federal Order.

The four Federal Orders paid by the "Advanced System" have the lowest butterfat levels. They are all paid for butterfat but the interest in increasing butterfat is apparently minimal, even with high butterfat prices.

|

| Table I - Butterfat Percent in April 2023 Compared to April 2022 by Federal Order |

The price of butterfat is a great incentive. As shown in Chart IV below, the price has doubled over the course of the last 23+ years. There was a significant drop in price during the COVID "stay at home" disruption, but otherwise, the growth in price has been steady.

|

| Chart IV - AMS Price of Butterfat |

|

| Chart V - Growth of Milk Protein Levels in Milk |

|

| Chart VI - AMS Price per pound fir Milk Protein |

|

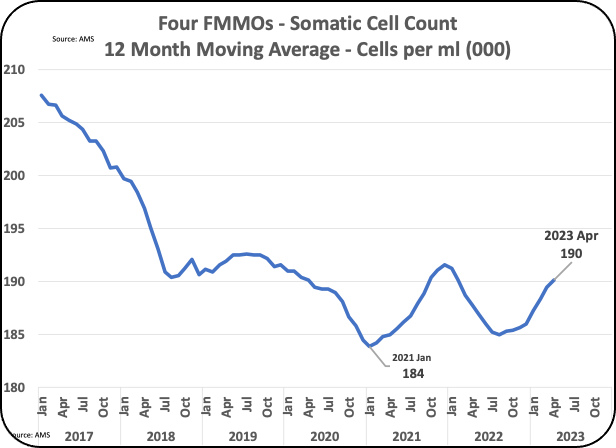

| Chart VII - Long-term USA Somatic Cell counts |