Class and Component milk prices continued their climb in October. The Class and Component price announcement can be reached at

this link.

Charts I and II below show the movement of prices of Class III milk, components, and the commodities that are used to calculate dairy prices. Chart I compares October prices to the prior month and Chart II compares the October prices to the prior year. Both show very similar patterns. Butterfat is down, milk protein is up, "Other Solids" are significantly down. and Class III milk is up. In the commodities that are used to price producer milk, cheese is up, Butter is down, dry whey is down, and nonfat dry milk is up.

The biggest influence on the Class III and milk protein prices is the price of cheese. See the

recent post for detail on the link between the price of Class III milk and the NASS cheese price. The NASS cheese price drives the Class III milk.

Cheese is up 25.6 percent vs. the prior year. That is a huge change considering that inventories have changed minimally.

|

| Chart I - Dashboard of Dairy Prices vs. Prior Month |

|

| Chart II - Dashboard of Dairy Prices vs. Prior Year |

Chart III below shows the 20-year movement of component prices. Milk protein prices have traditionally been higher than butterfat prices. Between

January 2017 and September 2019. butterfat was more valuable than milk protein. In the last two months, milk protein has again attained a higher price than butterfat.

|

| Chart III - Long-term Trends in Component Prices |

CLASS III MILK and CHEESE

The Class III milk prices (Chart II) reached $18.72/ cwt. in October. That is an increase of 36 percent since the start of 2019. That change is based entirely on the increase in the price of cheese (Chart V) which has increased 43 percent since the start of 2019. Just by comparing Charts IV and V, one can see the tight linkage between the cheese price and the Class III milk price.

|

| Chart IV - The Class III Milk Price over the Last Ten Years |

|

| Chart V - The NASS Cheese Price over the Last Ten Years |

Typically, cheese prices are determined by inventory levels. Inventory levels are down one percent from the same month in the prior year, and are even with the prior month (Chart VI). Based on the most recent data, cheese inventories are still at a high 36-day supply and are only one percent lower than the prior year. Comparatively. in December 2014, cheese inventories were at a 30-day supply.

|

| Chart VI - Cheese Cold Storage Inventory levels by Year |

The inventory levels can be expected to grow with increases in consumption, but as shown in Chart VII, those inventory levels are still above the trend line of normal growth.

|

| Chart VII - Long-term Growth Trends for Cheese Inventories |

BUTTERFAT

Butter prices are down 5 percent since the start of 2019. The drop-in butter prices were a surprise as cold storage inventory levels have not increased.

|

| Chart VIII - Butter Prices Over Ten Yeats |

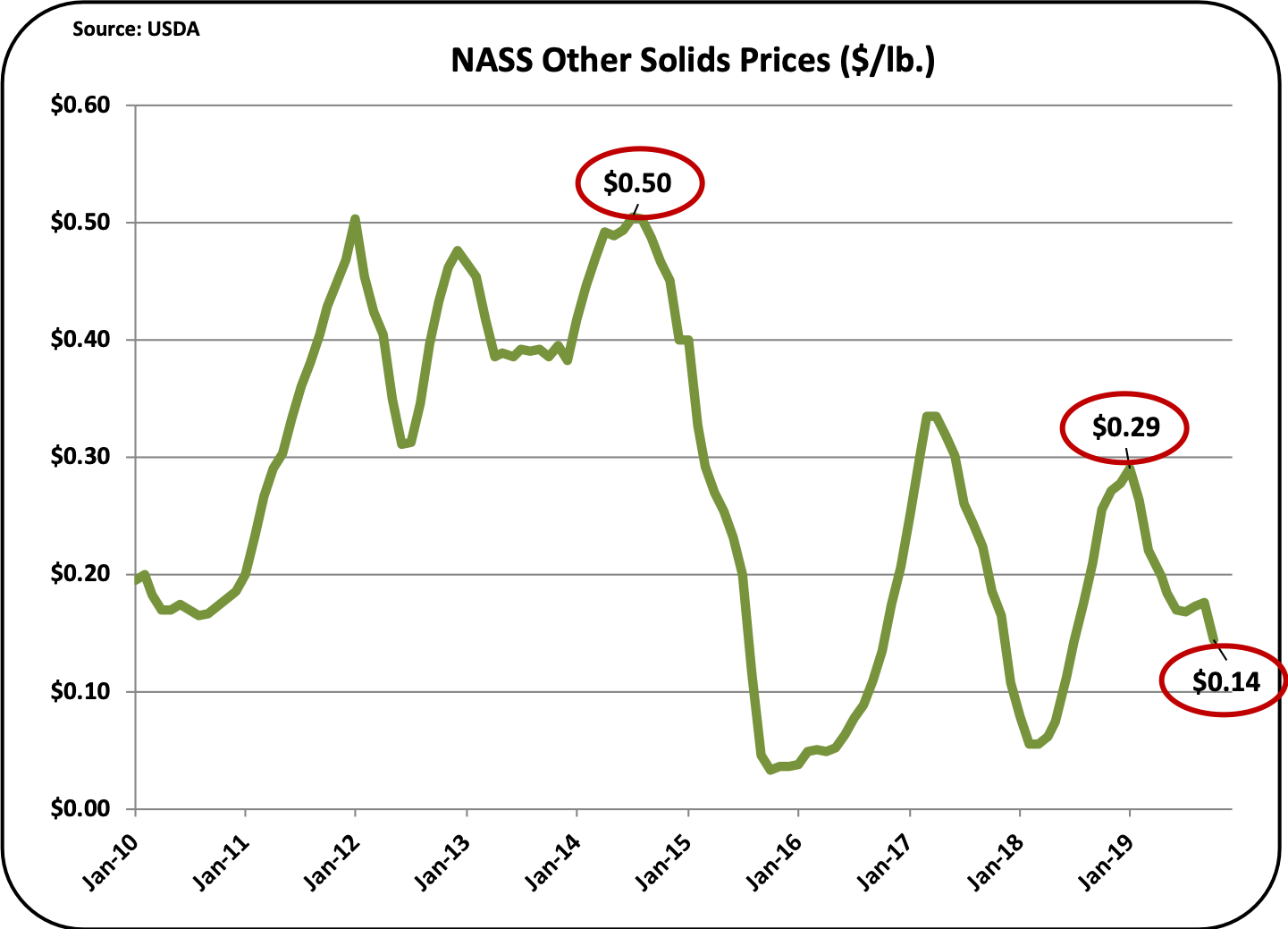

OTHER SOLIDS

The price of "Other Solids" is way down from the 2012 to 2014 period. From highs of $.50/lb. in the mid 2014, the October 2019 price is $.14/lb. The "Other Solids" price is driven solely by the price of dry whey.

|

| Chart IX - Other Solids Prices for Ten Years |

Dry Whey is primarily an export item. The current price of $.34/lb. is half of the high price in 2014.

|

| Chart X - Price of Dry Whey |

SUMMARY

Milk prices are up for only one reason, cheese prices are up. For a review of why cheese prices are up, read the

recent post to this blog. There is significant risk to the current and future expectations in cheese prices.

No comments:

Post a Comment