December Class and Component Prices were announced on January 3, completing the 2018 series. It was not a good year for producers. Class III prices ended the year at the second lowest price of the the year, $13.78/cwt. The Class IV price ended higher at $15.09/cwt., the highest class IV price for the year. Because the Class IV price was higher than the Class III price, it was also the basis for Class I milk pricing.

Butterfat prices were down 1.2 percent and cheese prices tumbled down 14.9 percent as cheese inventories remained very high.

|

| Chart I - Dashboard of Price Changes |

The Class III price has stayed in a very tight and low range for all of 2018. The lowest was in February at $13.40/cwt. and the highest was September at $16.09/cwt. There is no established trend higher or lower. The reason behind the low prices, high cheese inventories, continues to plague the value of cheese, and in turn, plague the Class III milk price.

|

| Chart II - Class III Milk Price |

For much of 2018, cheese production, Chart III, has been 4 percent or more above the prior year, Cheese disappearance domestically has been growing at about 2 percent and exports have not been growing at all for most of 2018. What is produced but not sold builds excess inventories (Chart IV). The glut of cheese is the biggest problem currently limiting producer milk prices. In 2017, the price of cheese averaged $1.64/lb. In 2018, the price of cheese averaged $1.56/lb., a decrease of 5 percent. Cheese production and inventory data are currently available only through October.

|

| Chart III - Cheese Production |

|

| Chart IV - Cheese Inventories |

The lower cheese prices also have an impact on the low Somatic Cell Count (SCC) adjustment paid to producers in the four middle U.S. FMMOs. The value of the SCC adjustment is based on the cheese price, and as the cheese price decreases, so does the adjustment. The adjustment begins to provide income when the SCC is below 350,000 cells per milliliter. Current averages for SCC are around 200,000 cells per milliliter. At current cheese prices this is worth only about $.10/cwt.

Nonfat

Dry Milk (NDM) prices have improved slightly in 2018 ending the year at

$.90/lb. For the year 2018, the NDM price was 8 percent lower than the

prior year price of $.87/lb. However, by year-end 2018 the December price

has recovered to $.90/lb. NDM includes Skimmed Milk Powder (SMP) which is

primarily an export item. The majority of NDM/SMP is exported and the

price is based on supply and demand in the international markets. Most of

the U.S. exports go to Mexico.

The NDM

price is the basis for the Class IV skim milk price. During the year 2018, the Class IV skim milk

price has increased from $4.71/lb. in January to $6.54/lb. in December, a 38

percent increase. The current price is still way below historic price levels.

|

| Chart VI - NDM Prices |

When the price of Class IV milk is higher than the price of Class III milk, the Class IV price becomes the basis for the skimmed milk price of Class I & II. In turn, this can increase the "Uniform" milk price (weighted average price) above the Class III price resulting in a higher Producer Price Differential (PPD) payment to producers. While these are typically small amounts, in a time of tight prices any "small amounts" are appreciated. The PPD is larger in FMMOs like the Northeast with more Class I milk. In December, the PPD for the Northeast Federal Order was $2.18/cwt., while the PPD for the Upper Midwest, which has a very limited Class I business, was $.30/cwt.

Butter prices have been very stable in 2018. They have ranged by only 13 percent, with a low of $2.11/lb. and a high of $2.38/lb. The prior year range was 26 percent, twice the 2018 price range. This signals a significant reduction in butter pricing volatility. On the average, the butter price was 3 percent lower in 2018 compared to the prior year and ended the year at almost exactly at the same price as the prior year.

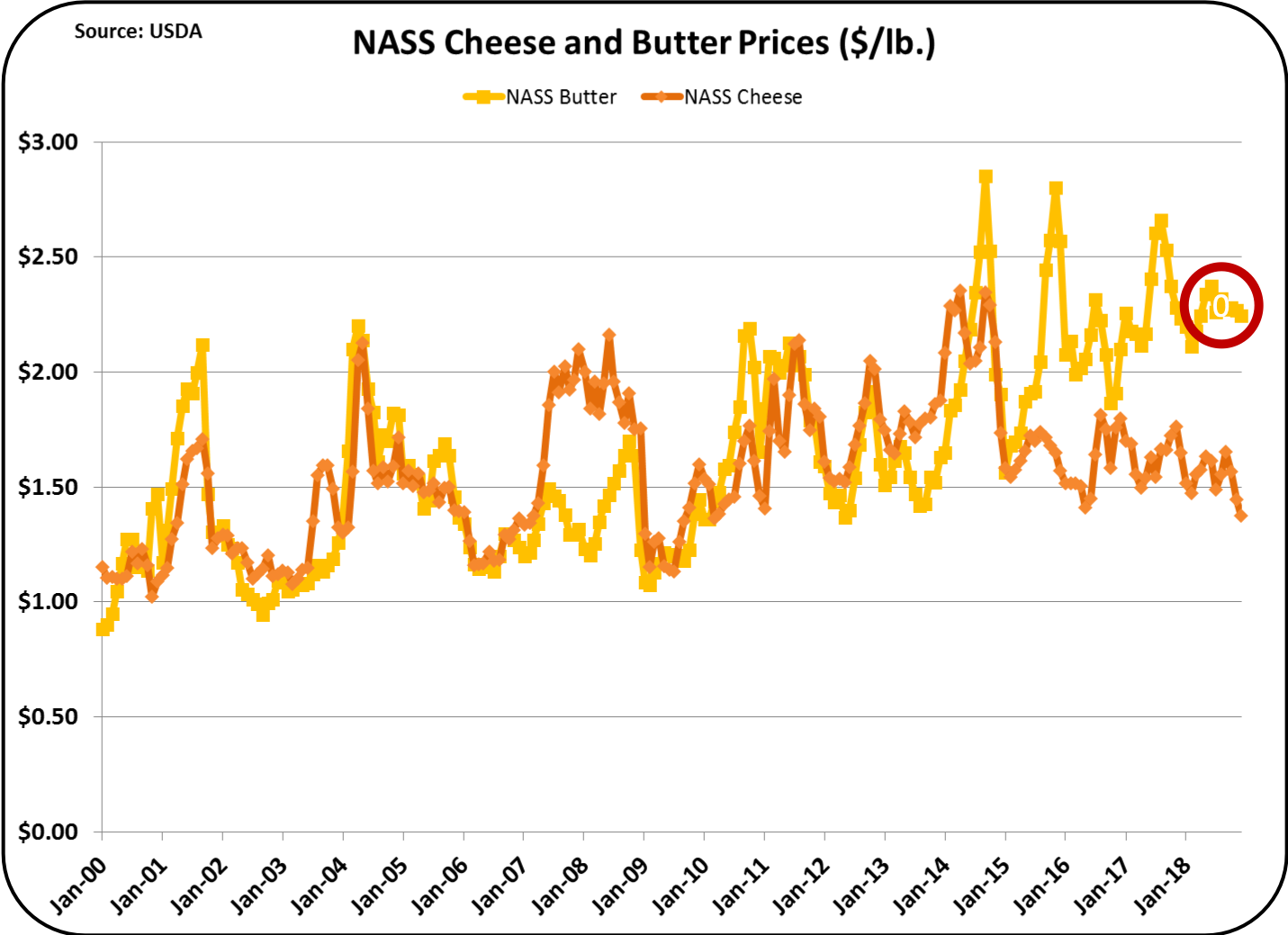

The spread between butter and cheese prices reached $.87/lb. in December as cheese prices hit a low point for the 2018 year (Chart VII).

|

| Chart VII - Prices of cheese and Butter |

Butter production has increased in the last three years to meet demand (Chart VIII). As a result, inventories have increased to reasonable levels as well. Another indicator is exports. Although exports are still minimal, they have increased from prior years. As covered in the prior post on imports, imports of "Irish butter" have increased significantly in 2018, also taking the heat off of the tight butter inventory levels. It would appear that there might be some softening of U.S. butter prices in 2019.

|

| Chart VIII - Butter Production |

In summary, 2018 has been a tough year financially for milk producers. While market volatility of butter prices has settled down, the extremely high inventories of cheese have depressed cheese prices. Cheese prices are the primary determinant of the Class III price.

Will you be talking about this change in FMMO pricing as described here...

ReplyDeleteFederal Order pricing provisions have been amended to change the class I price mover to the average of the monthly class III and IV prices, rather than the higher of the two. To compensate for the fact that this average will always be lower than the higher of the two, an adjustment factor of $0.74 per hundredweight (cwt) will be added to the average of the two classes. The exact impact this change will have on farm milk prices is dependent on the relative value of Class III and Class IV milk going forward, but the intent is that these slight adjustments to the farm price will make hedging strategies easier. The USDA has until the end of March 2019 to implement this change.