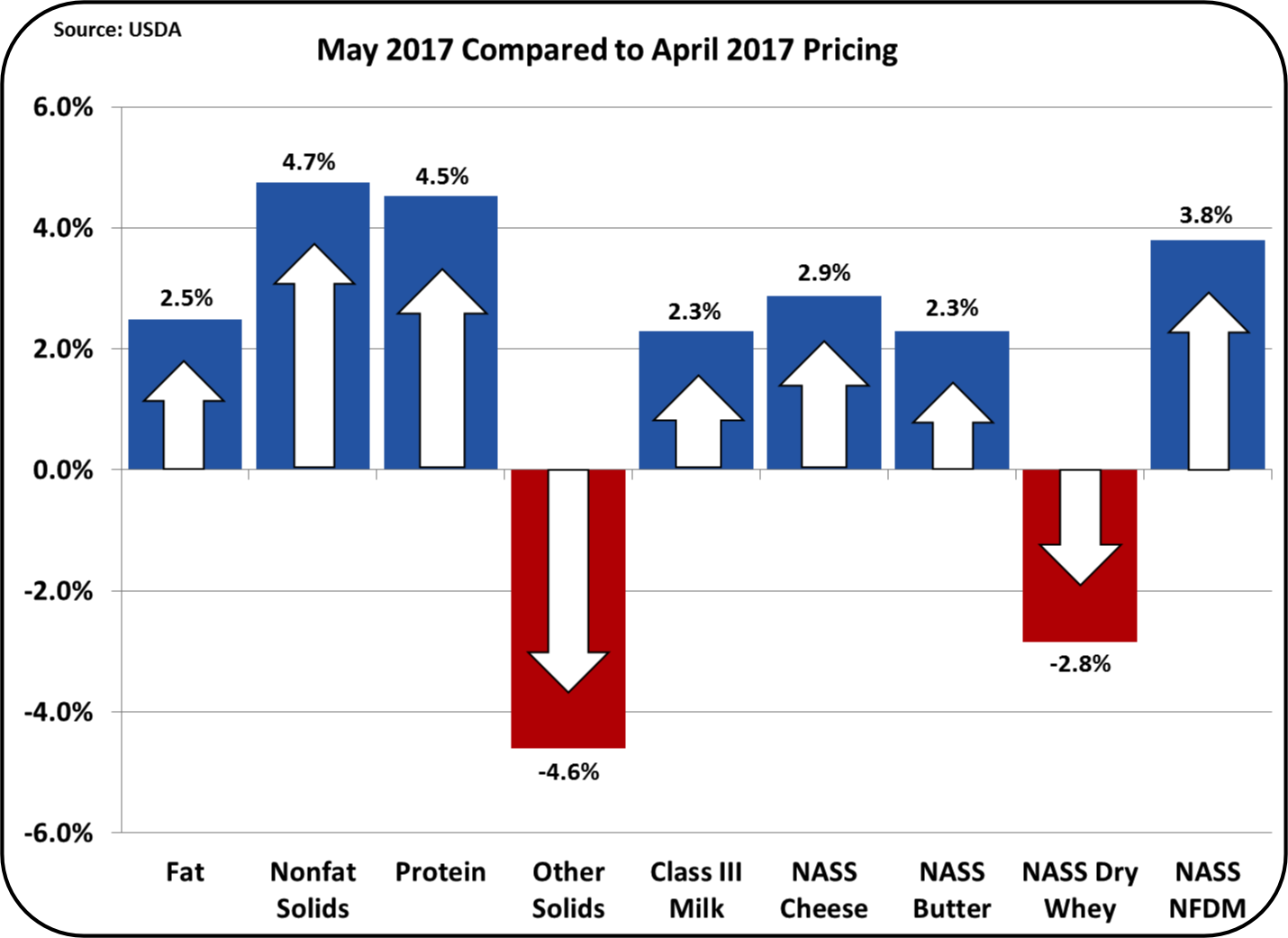

The long-term trends remain consistent with prior 2017 months with milk protein worth less than butterfat. Although Other Solids were below the prior month they remained near their current prices. Dry whey has recovered nicely in 2017, but is still below the 2014 record prices. The price of dry whey us determined in the international markets.

A closer look at the long-term trends shows a two year continuance of butterfat being more valuable than milk protein. With pressure on butter inventories, caused by low production and increased domestic consumption ( See prior post on consumption trends), butter and therefore butterfat continues to maintain high prices. While a high price for butterfat seems like a good scenario for producers, it has a very minimal impact on the Class III milk price.

Butter inventories have returned to prior year levels at end of April. Butter production is running at about the same level as the prior year. Domestic consumption continues and the increased demand is being met with butter imports. Exports remain near zero.

The high price of butter can be expected to continue throughout the remainder of 2017 as demand continues to grow and production continues at 2016 levels.

Cheese showed a nice increase in price in May, but inventories remain troubling. While there is increased consumption and increased exports, production levels remain above demand and inventories continue to grow to record levels. Domestic consumption cannot reduce this inventory. With an increasing milk supply, production will remain robust. A spike in exports is really the only solution. Exports (and imports) will be covered in the next post to this blog.

Class IV milk can move the uniform milk price significantly (see this post for an explanation.) Class IV skim milk prices are determined by the price of NDM, which in turn is determined by the international price of NDM. However, while the price of NDM has slightly increased from 2016, it is still way below the 2014 highs.

Because of this, the Class IV price remains well below the Class III price, and will probably remain there for the balance of 2017. Therefore Class I milk prices will remain linked to the Class III prices. While NDM export volumes have been increasing to record levels, the price will probably remain low.

Probably this most important item to watch is exports of cheese. Cheese pricing is the most important variable in calculating the Class III price. Europe is the world's largest dairy exporter and has enjoyed an exchange rate advantage in the international markets. That exchange rate is now shifting toward a stronger Euro. A continuation of this exchange trend will make European products more expensive compared to the U.S. New export/import data will be available soon and will be covered in the next post to this blog.

No comments:

Post a Comment