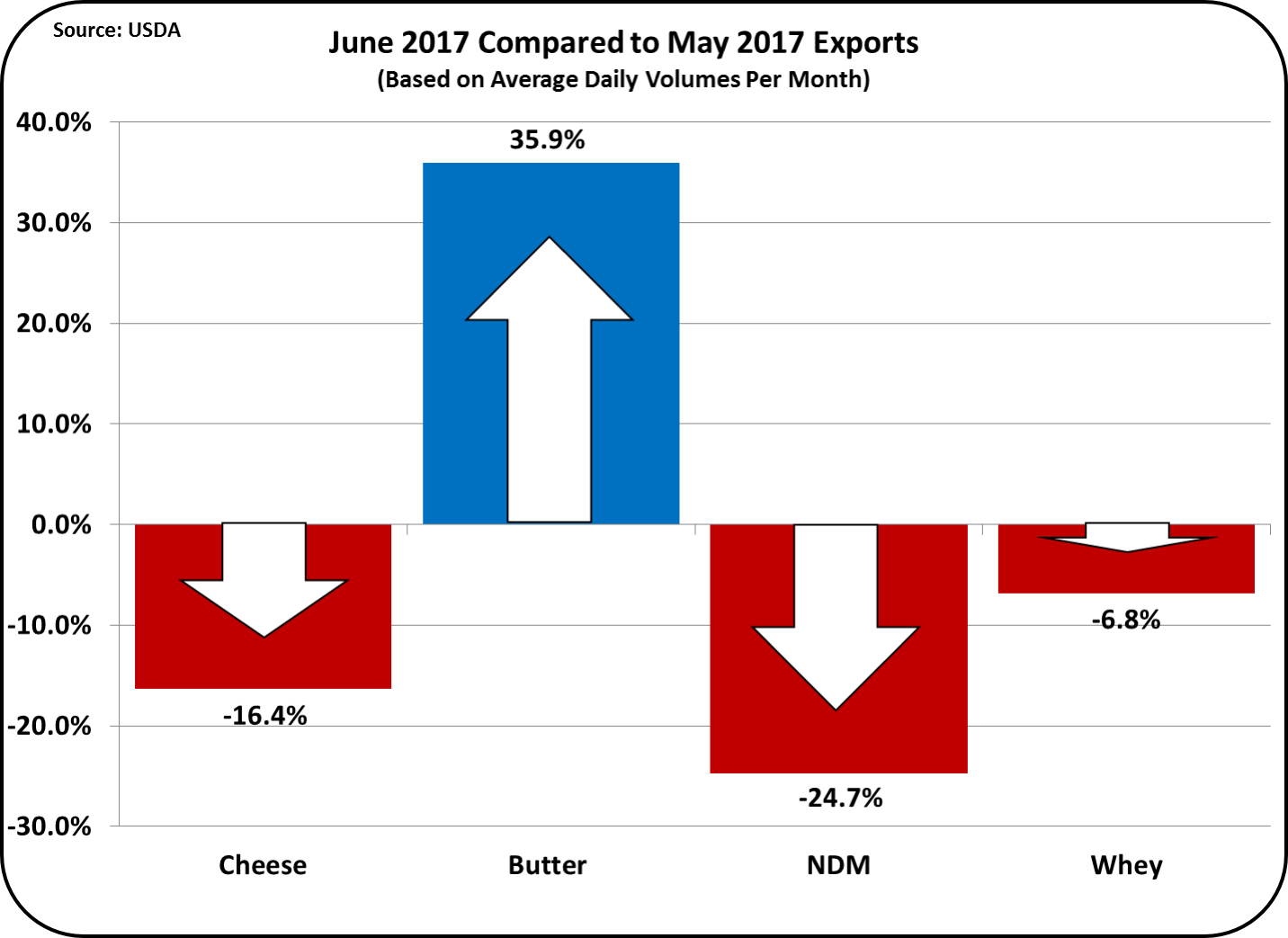

Dairy exports showed some weakness in June, but from a broader perspective the first half of 2107 was up considerably over the prior year. Butter exports were up 35.9% from May, but it was on a very small base. With the domestic shortages and tight inventories, it would be difficult to export any significant amount of butter. Exports of cheese, nonfat dry milk (NDM), and dry whey were all down versus the prior month.

|

| Chart I - Export Changes from Prior Month |

As mentioned in the

July 9 post to this blog, long-term increases do not typically occur with increases each month. Long-term increases always have ups and downs. The upward trend for cheese exports started in October 2016 and has continued to grow reaching a near record level in May 2017. If there is another downturn in August, that could be concerning, but the one month decrease is normal for an improving market. There are now nine months of data supporting an upward trend in cheese exports.

|

| Chart II - Monthly Exports of Cheese |

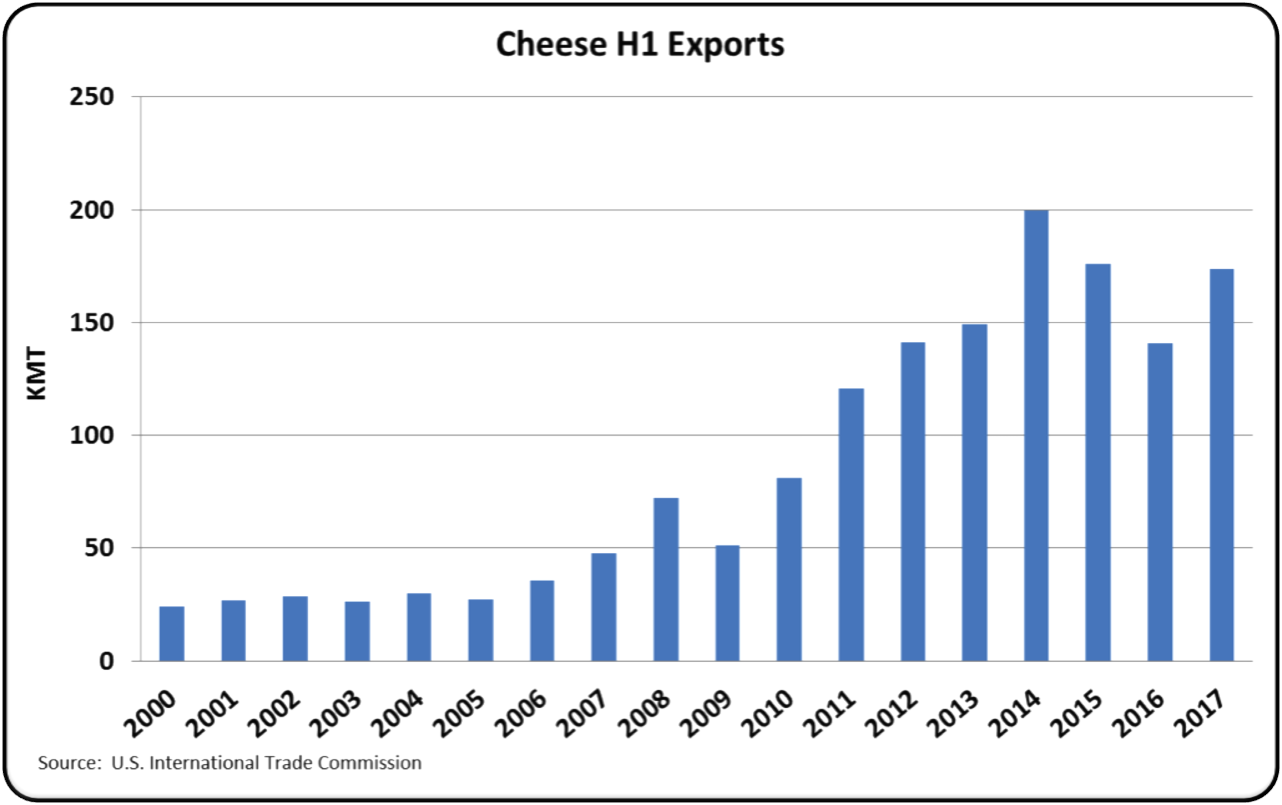

Cheese exports for the first half of 2017 were close to the second best ever. Cheese exports are the most important parameter for insuring that there is a sufficient market for the cheese being produced. Without a sufficient market, inventories will increase and prices will fall. With lower cheese prices, Class III milk prices will also fall as well as the uniform milk price.

|

| Chart III - Cheese Exports for January through June |

NDM exports are the backbone of U.S. dairy exports. It is by far the largest export category and the U.S. is the world leader in NDM exports (see

prior post). June exports fell significantly. As with cheese, one month of data, although troubling, does not define a long-term problem.

|

| Chart IV - Monthly Exports of NDM |

For the first half of 2017, exports of NDM were about even with the record year of 2014. Unfortunately, prices were much lower than 2014, but the volume has helped in keeping demand for dairy products closer to supply.

|

| Chart V - NDM Exports for January through June |

Exchange rates are continuing to show a weaker USD, which will help increase exports by making U.S. products less expensive in the international market.

When the chart charts below show an increase, the USD is weaker and U.S. export products are more competitive. The two largest export competitors in the international markets are Europe and New Zealand. (More detail is available in the

July 28 post.) In the two charts below, there is a trend toward a weaker USD and a stronger Euro and NZD.

|

| Chart VI - Exchange rates for the USD vs. the Euro |

|

| Chart VII - Exchange Rates for the USD vs. the NZD |

Mexico is by far the largest export market for U.S. Dairy products. The Mexican Peso is gaining strength against the USD, which in turn is making U.S. dairy products more financially attractive in Mexico. This is another very positive sign for U.S. dairy exports.

|

| Chart VIII - Exchange Rates for the USD vs. the Mexican Peso |

Exports to Canada are not typically significant as Canada is not a NAFTA open border for dairy products. However there has been a great deal of press concerning a possible renegotiation of NAFTA. It seems unlikely that Canada will open their market for dairy imports. However, if this did happen it could have a very strong and positive impact on U.S. dairy exports. The exchange rate of the USD/CAD could be very important and it is currently showing a weaker USD and a stronger CAD.

|

| Chart IX - Exchange rates for the USD vs. the CAD |

While June exports has some disappointing analytics, the longer-term view shows very positive trends. The data for July, which will be ready in a few weeks, should tell a lot.

No comments:

Post a Comment