|

| Chart I - Price Changes from Prior Month |

Cheese production is strong in spite of growing inventories. When there is too much milk, where else can it go? Cheese production is outstripping domestic consumption and exports. As a result, inventories are rising.

|

| Chart II - Cheese Production |

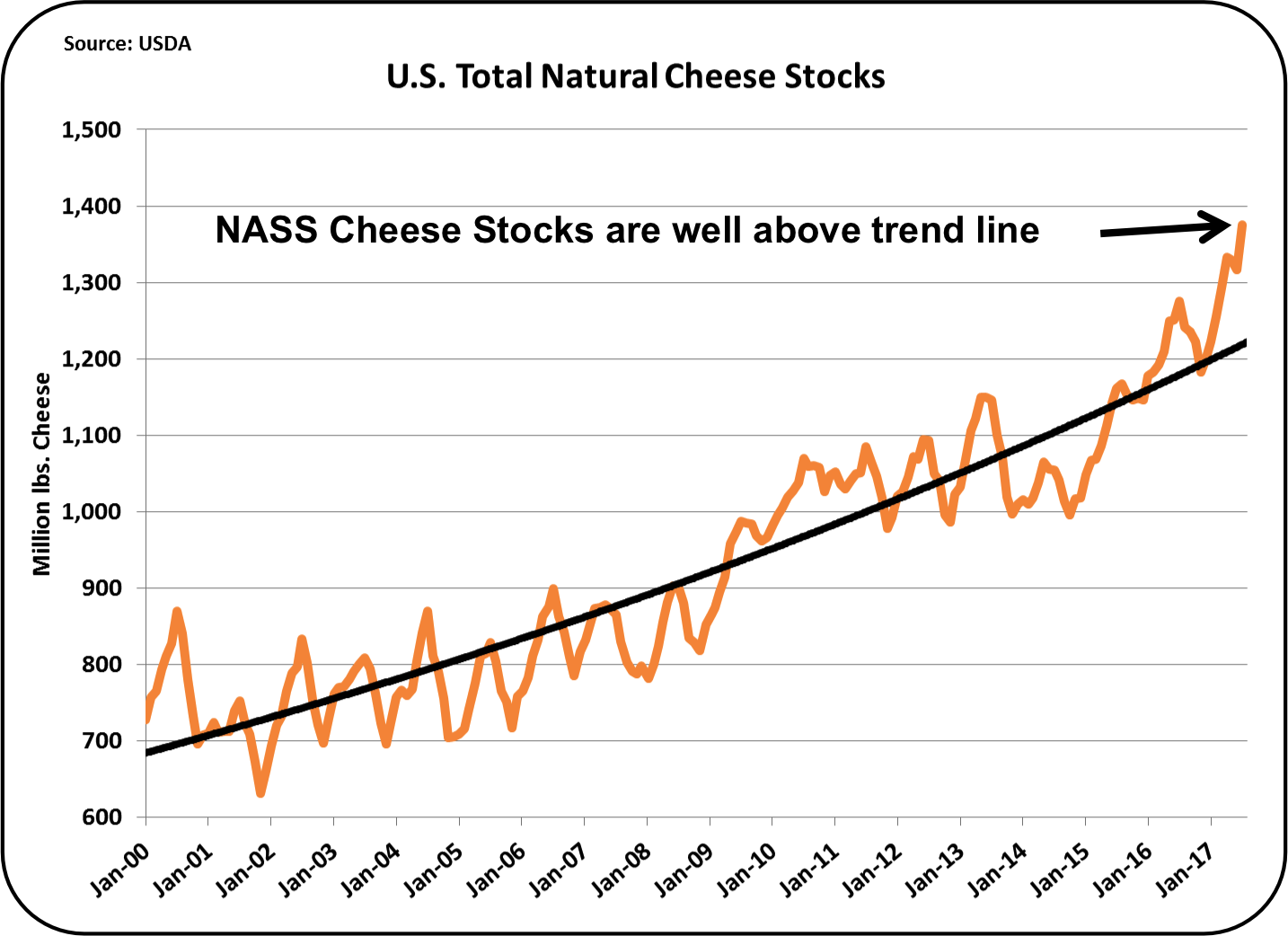

The severity of the inventory increase is displayed in the two following charts. Cheese stocks need to increase over time with the increase in consumption. The growth in inventory is needed to provide sufficient stocks to manage the demand. The chart below shows the growth in cheese stocks since 2000, which is consistent with the growth of consumption plus exports. However, the stocks are currently well above the long-term trend line. The inventory is at a record level above that trend line.

Chart III - Long-term trends in Cheese Stocks

Chart IV below compares year-by-year levels of cheese inventories on a month-to-month basis. July ending data shows a significant and concerning swelling of inventories.

|

| Chart IV - Cheese Inventories |

In spite of this, the NASS cheese price did go up in August to $1.67/lb. The most recent CME cash prices as of September 1 were $1.54/lb. for blocks and $1.52/lb. for barrels. These numbers signal a potential strong drop in the NASS cheese price for September and, therefore, a strong drop in the Class III milk price.

Butter inventories remain tight. Demand for butter remains strong in spite of the high retail prices. The NASS butter price rose only slightly in August to $2.67/lb. from $2.62/lb. the prior month.

|

| Chart V - Butter Inventories |

Production of butter is running lower than prior years in spite of the higher demand for butter. The shortfall is being made up with butter imports, primarily from Ireland. There is strong demand for butter from Ireland, which is considered premium butter by many consumers. It is "cultured" and has a slightly stronger flavor and a higher melting point. There will be more on this in the next post, which will analyze export/import data.

|

| Chart VI - Butter Production |

The price of dry whey, the basis of "Other Solids" pricing lost 3.7% in August, but remains at a mid-range level. Therefore, the price of "Other Solids" remains at a respectable level of $.24/lb.

|

| Chart VII - Dry Whey Prices |

The dairy commodity markets remain turbulent. Articles on the high wholesale and retail price of butter are everywhere. It is not just a domestic issue, but a global issue. As covered in the prior post, butter prices mostly just move dollars from milk protein to butterfat or vice-versa. The dominant force for milk prices is the wholesale cheese price. The change in August was welcomed, but may be short lived. The low spot market prices quoted above, are not indicative of the futures cheese market, which is quoting continuing prices in the $1.60/lb. range for the remainder of the year. This will only be possible if cheese exports quickly pick up. New data on exports will be available next week and will be covered in the next post to this blog.

No comments:

Post a Comment