May dairy exports had some good points, but when it came to the major items that really influence producer milk prices, there was not much good news.

The most important export product for milk prices is cheese. Cheese exports were down, not up.

While the overall volume of exports was up 18% from the prior year, the dollar value of exports were just even with the prior year. The main reason is that what was exported was low value products like Nonfat Dry Milk (NDM) and dry whey. While butter exports were up over the prior year by a huge percentage, butter exports are so small that a big percentage increase is almost nothing.

Were the Mexico tariffs on cheese to blame? The answer is, probably not, as the tariffs were announced in June and this post is reviewing May exports. The fear of a June tariff could have played a roll in accelerating May purchases, but that did not happen.

Cheese is by far the most important commodity influencing Federal Milk Marketing Order milk prices. Cheese prices have been low because cheese inventories have been very high. Supplies are outweighing demand. Exporting significant quantities of cheese would have helped reduce the swollen inventories. Unfortunately, May cheese exports (Chart I) were down from the prior month of April, and April was already down from March. May 2018 cheese exports were also down from the year ago May volumes. Not much good news here.

|

| Chart I - Cheese Exports |

To add to the inventory issues, cheese imports (Chart II) were up! This is the third consecutive month of increases in cheese imports.

|

| Chart II - Cheese imports |

When combining lower exports and higher imports, net cheese exports (Chart III) show a decline. The

prior post showed and discussed the alarming growth in cheese inventory. Producer milk prices will not improve until these inventories are reduced.

|

| Chart III - cheese Net Exports |

The biggest export volume mover is NDM. While NDM volumes are up substantially from the prior year, but in May, they did drop from the prior month. Nothing climbs in a straight line, so there is not much concern here about the NDM export volume. However, there should be concern about the NDM price of $.82/lb. Big volume increases in a competitive market require low prices.

|

| Chart IV - NDM Exports |

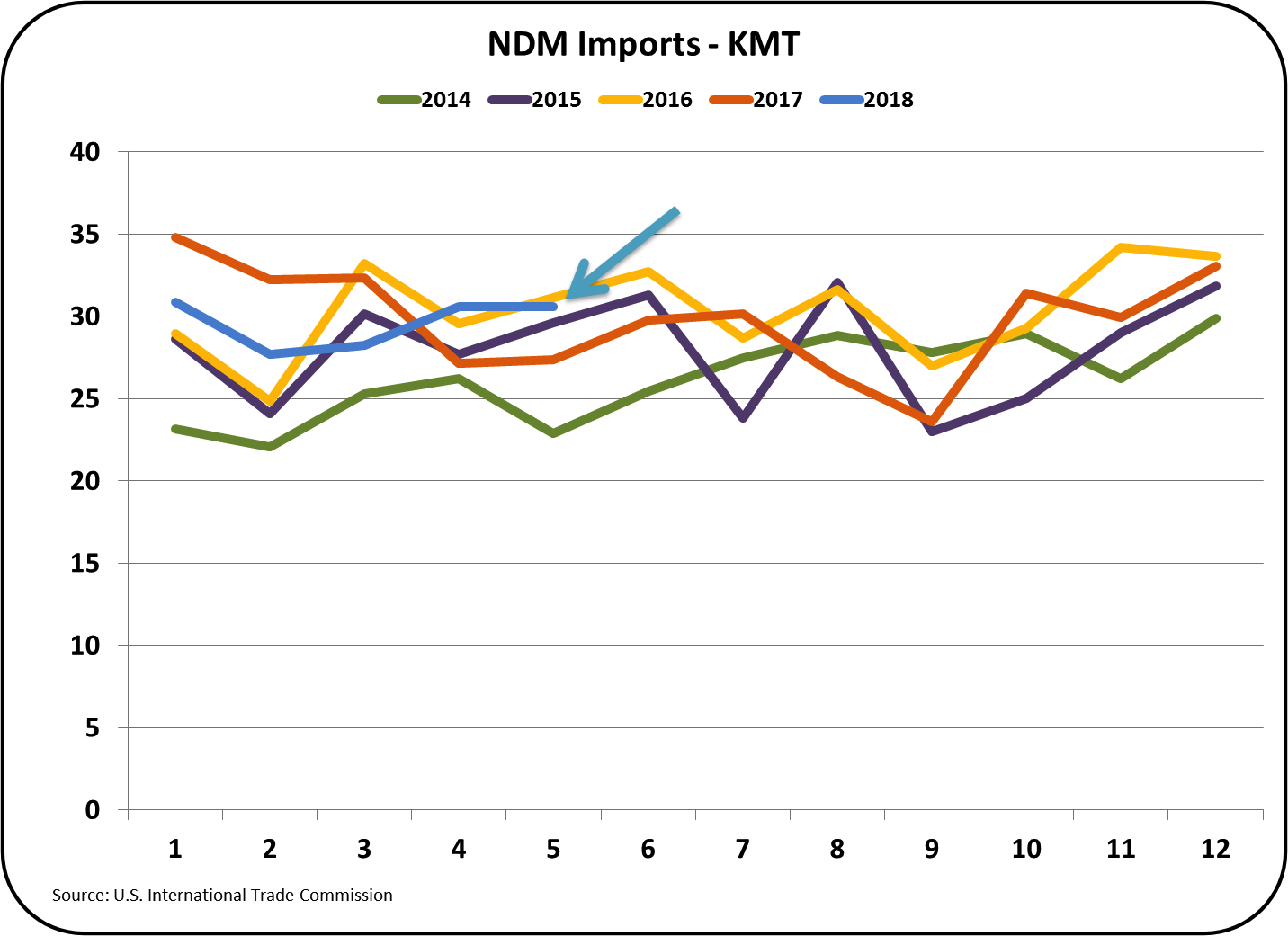

What is surprising is that NDM imports are also strong. Typically, when exports are strong it means that International prices favor the U.S. and imports fade for the same reason. That is not happening.

|

| Chart V -NDM Imports |

The largest source of NDM entering the U.S. is Canada (Chart VI). Canada has the same problem that the U.S. has in that increased butter consumption leaves a lot of NDM available. The nearest export market for Canada is the U.S. Canada must sell this excess NDM at a compromised price.

|

| Chart VI - NDM Exports by country |

So where does that leave the NDM export effort? Right now, NDM net exports are down from the prior month and just barely ahead of the 2014 levels. The logical thinking is that the booming exports of NDM are getting rid of a lot of the excess milk in the U.S. However, imports are at a level of almost 50% of exports, diminishing the impact of exporting nonfat dairy solids (Chart VII).

|

| Chart VII - NDM net Exports |

Dry whey exports are doing well. They are currently reaching the levels of 2014, when U.S. exports were setting records.

|

| Chart VIII - Exports of Dry Whey |

There is a significant mix problem with the U.S. Dairy exports. Cheese exports are down. NDM and dry whey exports are doing well compared to prior years. The problem is that cheese is expensive, and NDM and dry whey are very inexpensive. For the month of May, the NASS price for cheese was $1.61/lb. while NDM was valued at $.82/lb. and NDM was valued at $31/lb. The current mix provides lower total revenue despite the increased volume. More cheese exports is what is needed to improve producer prices..

The export emphasis needs to focus on cheese to provide a pay back for the producers who financially support the USDEC.

No comments:

Post a Comment