In the prior two posts the 2022 milk Class prices were covered and the 2022 component prices were covered. The component prices are used to establish the milk Class prices. In this third post, the commodities that are used to calculate the component prices will be covered. In a sense, this is the third level of peeling the milk price onion down to see where and why producer milk prices have moved and where they might be going.

There are four commodities that are used to price components, and they are butter, cheese, dry whey, and nonfat dry milk. In three of the four commodities reviewed below, inventories are low to normal. Scarce inventories will keep prices reasonably high. The one commodity with a huge inventory is dry whey and for that reason the value of dry whey is and will remain low. Other solids pricing, which is based on the price of dry whey, is not a major contributor to milk prices.

BUTTER PRICES

The first to be reviewed is butter. Consumption of butter has been growing at around two percent annually. In the last two years, retail butter prices have increased significantly, and this may be dampening demand. Wholesale butter prices charted below have seen tremendous continuing price increases, setting new record highs every month through October 2022. There has been a little drop in the wholesale butter price in November and December 2022.

|

Butter Prices

|

The increases in butter prices are caused by basic supply and demand. Butter wholesale inventories have been decreasing and still are. In November, inventories fell further. November's inventory of 200 million pounds is down five percent from the prior year and the prior year at 210 million pounds was already very low. The year to prior year decline has been continuous for the last 16 months.

|

| Butter Wholesale Inventory |

A major part of the problem is that butter churning is down. While year-to-year production should show increases to match growing domestic consumption, production is falling. November 2022 did provide a slight increase in production from the prior month, but it is still a very low production volume. The main culprit is a lack of milk combined with increased butter exports. While exports are still small compared to domestic disappearance, they have been growing for the last two and a half years. Milk producers and butter processors struggle with labor shortages, high feed costs, and uncertainty for the future. For more information on butter pricing,

click here.

|

| Butter Production |

CHEESE PRICES

Cheese prices are the major factor in pricing milk protein. The "cheese" price announced by the Agriculture Marketing Service (AMS) is based only on Cheddar cheese wholesale prices. The price has been escalating in 2021 and 2022. Every month of the year 2022 is higher than the same month of 2021.

|

| Cheese Price

|

Cheddar cheese inventories are not available publicly, but Cheddar cheese makes up about 70 percent of American cheese. Inventories of American cheese, shown below, were highest in mid 2022 but have fallen to a low by November 2022. Low inventories support higher cheese prices and higher protein component prices.

|

| American Cheese Inventory |

Production of Cheddar cheese, shown below, has been declining in 2022. The low production rate has stretched inventories and supported good Cheddar cheese prices. The decreased production has been caused by a shortage of raw milk, labor shortages, and uncertainty.

|

| Cheddar Cheese Production |

DRY WHEY

Other solids are priced based on wholesale dry whey prices. The chart below shows the rise and fall of dry whey prices. They have been very volatile, especially in 2022. Dry whey has dropped from $.79 per pound to $.46 per pound, a 42 percent fall.

|

| Dry Whey Prices |

Dry whey inventories are high compared to 2021. In early 2022, inventories grew. Because cheese production continues to grow annually, that leaves more whey to find a home. Ninety eight percent of the dry whey is consumed by people, not animals. About half of dry whey is exported and is subject to international fluctuations. This includes whey permeate (whey with no protein). a large part of which is sold to China for their swine industry.

|

| Dry Whey Inventory |

Dry whey production has been volatile, but at the end of the year, it remains even with the prior year.

|

| Dry Whey Production |

NONFAT DRY MILK

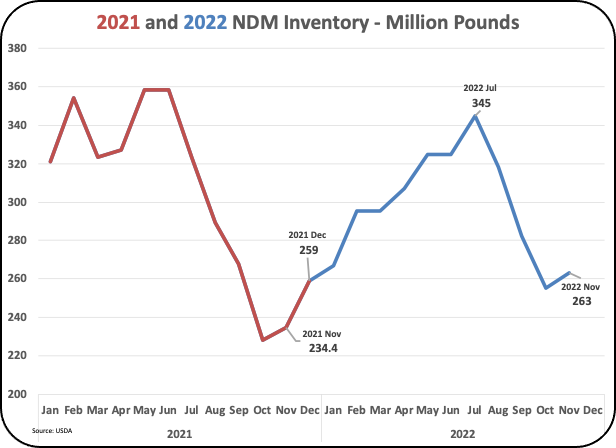

NDM prices have increased and decreased. At year end NDM prices remain even with the prior year. NDM is used to price the skim milk for Class IV. Because skim Class IV prices are used in valuing skim Class I and skim Class II milk, they are a major factor in producer milk pricing.

|

| NDM Prices |

Inventories of NDM milk are ending even with the prior year. Without a surge in inventories, prices should be stable.

|

| NDM Inventory |

Production of NDM is neither high or low. Over 70 percent of NDM is exported, so demand and prices can vary with exchange rates and international competition.

|

| NDM Production |

SUMMARY

As mentioned at the top of this post, the inventories and production of the major commodities used to price milk components show no signs that would weaken producer milk prices. Dry whey is an exception and currently has very high inventories. The price of dry whey is used to price "Other Solids" but has little impact on overall producer prices.

No comments:

Post a Comment